Maybe it was a phone call from a doctor.

For your family, it might have been your husband walking in from work and telling you he had been laid off.

Some people discover it when they do the daycare math and realize the second paycheck is almost entirely paying for childcare.

Important: Only 23% of U.S. workers have access to paid family or medical leave through their employer. For most households, a family or medical emergency can trigger an immediate financial transition.

Source: Bureau of Labor Statistics

Maybe it was a parent who needed more help than anyone had planned for, or a move across the country for his career where yours quietly got left behind.

Whatever it was, there was a moment. And after that moment, everything about how your household finances were managed had to change.

This post is for anyone in that moment right now, or anyone who wants to be ready before it arrives.

When It Happened to Us

My husband was serving in the Army Reserve and staying home with our son. For about nine months, we had already been living on one income while he cared for our baby. Then he was called to active duty for a special assignment. Suddenly, we needed childcare. We found a daycare near my job and thought we had solved the problem.

Something Didn’t Feel Right

A few days later, something felt wrong. I called the daycare. Everything was supposedly fine. But I could not shake the feeling that something was not right.

I asked my supervisor if I could leave work to check on my son. The answer was no. I said, write me up if you need to. I am leaving.

When I arrived, the daycare provider told me he had a small fall and slipped on his sandals. She said he was lying down in the back room.

As we spoke, I could hear my son calling, “Mommy, Mommy” from another room. The provider assured me he was fine, but something didn’t seem right.

I walked past her and went to the back room myself. That’s when I noticed a knot on his head. His voice was hoarse from crying.

As I was leaving, several little girls followed me outside. One of them asked, “Do you want to know what really happened to your baby?”

They told me he had been crying for a long time. At that moment, I knew there was more to the story than a simple fall.

One of the little girls explained what had happened. Another child, only about five years old, had been trying to comfort him because he was crying. Her intentions were kind, but she couldn’t hold him and dropped him.

I took him straight to the hospital. He had a mild concussion.

That was the turning point. Not because the concussion automatically made us a one-income family. It did not. The turning point was that it forced us to stop and ask questions we had not been asking.

The Questions We Could No Longer Ignore

Now, that moment did not automatically make us a one-income family. We found a much better childcare arrangement, and I continued working.

But the daycare incident forced us to ask questions we had been avoiding. If my husband stayed on active duty full-time, would it still make sense for me to keep working? What would our finances actually look like if we relied on military income alone?

Those are not easy questions. But they are the right ones.

At the time, I had a good job. The company paid substantial bonuses, and for several years those bonuses added thousands of dollars per month to our household income. But we had not built our lifestyle around those bonuses. Instead, we used them to pay off debt. We paid off cars. Other debt disappeared along the way. Our mortgage stayed manageable.

Without realizing it, we were creating the flexibility that would become one of our greatest financial advantages.

Three months after the daycare incident, my husband transitioned to active duty full-time.

After running the numbers, we decided that I would leave my job and stay home with our son.

The Army relocated us to Georgia, and I looked at returning to work after the move.

But the jobs available were not comparable to what I had left behind.

The pay was lower, the commute was longer, and none of them offered the flexibility our family needed.

When we ran the numbers honestly, it still did not make sense.

The Decision Was Made Long Before We Made It

Looking back, the decision was not made in a single day. It was made over years of paying off debt, avoiding lifestyle inflation, and creating options before we knew we would need them.

And that is something many people misunderstand about one-income families. Most of us do not make this decision once. We make it repeatedly as life changes and circumstances shift. Each time, we stop and ask what matters most for our family right now.

Our story involved a military assignment and childcare. Yours may look completely different. A layoff. A parent who needs care. A relocation. A health issue. A divorce. The circumstances are different. The financial question is often the same.

The Question Nobody Asks Until They Have To

Most financial advice treats these situations as separate problems with separate solutions.

There is layoff advice. New baby advice. Caregiving advice. Divorce advice.

Each has its own experts, its own resources, and its own corner of the internet.

But underneath every one of these situations is the same financial question:

What does your household actually look like on one income?

Most families never ask that question until life forces them to. Not because they are careless with money. Not because they have done anything wrong. Two incomes feel stable. And stable feels permanent. Until it isn’t.

The families that navigate financial transitions most successfully are not always the highest earners. They are the families who already understand their numbers, know what their household truly costs to operate, and have a plan before they need one. The transition may be different. The financial question is the same.

Our story involved a military assignment and a daycare incident. Yours may look completely different.

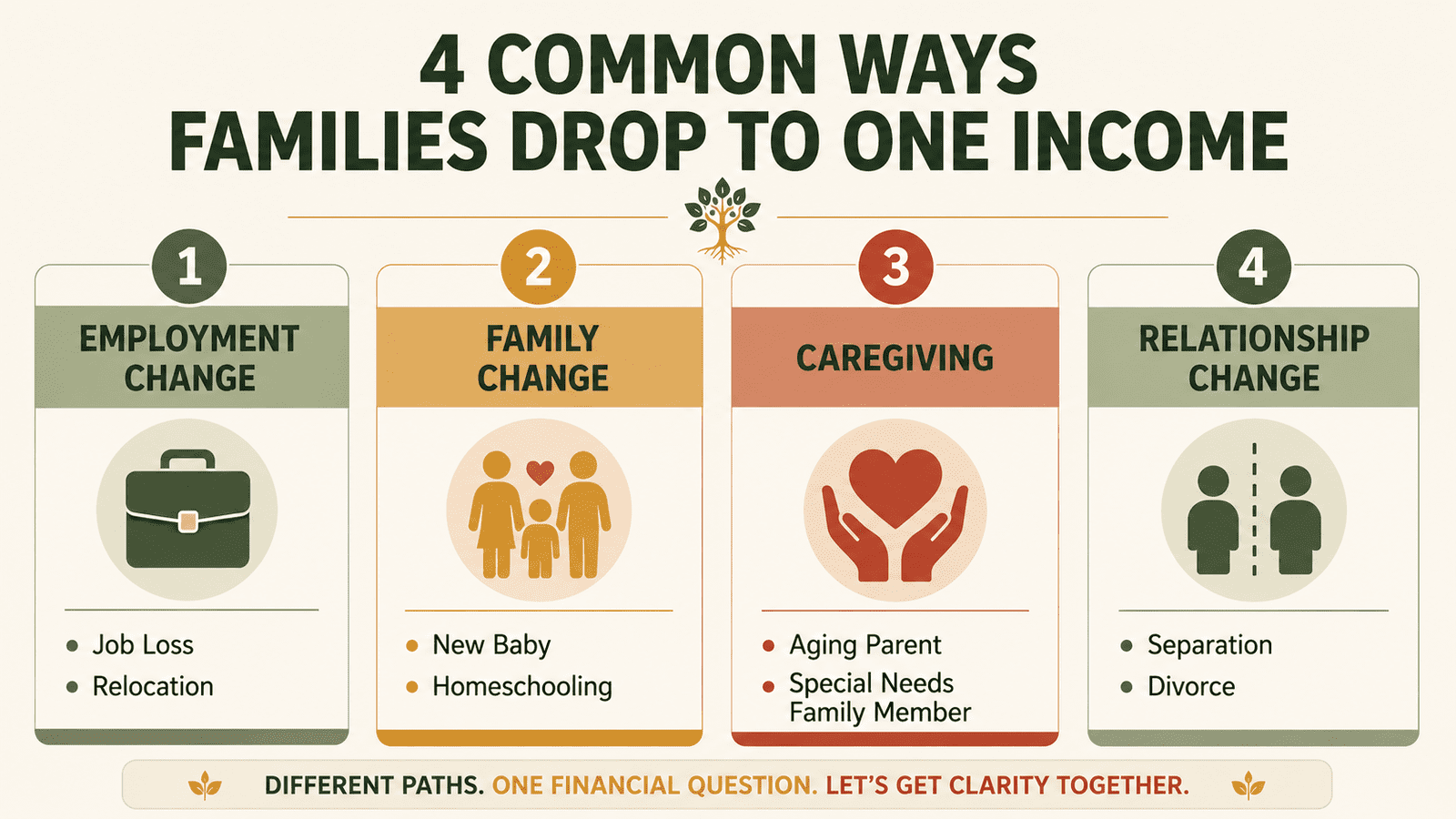

There are four common ways families drop to one income

Financial transitions rarely look the same from one family to the next. Some arrive suddenly. Others develop over months or years. Yet most fall into four broad categories. Knowing which one you are facing can make it easier to evaluate your options and plan your next steps.

Employment Changes

Job Loss or Relocation

For many women in their 30s and 40s, the income that disappears first belongs to their partner. A layoff hits immediately and hard. Relocation is different: his company offered a promotion, you said yes together, and then you discovered that your professional network, your seniority, and your license, in some cases, did not transfer automatically to the new city. The financial gap from relocation often shows up three to six months later, once the excitement settles.

Family Changes

A New Baby or Homeschooling

The childcare calculation is rarely impulsive. Most of the time, it follows a very specific question: what is my paycheck actually contributing after childcare, commuting, meals, and work expenses? When families run those numbers honestly, the margin is often smaller than expected. Sometimes it disappears entirely. Homeschooling follows a similar pattern, a chosen transition that still requires real financial preparation. The number of homeschooling families in the US roughly doubled between 2019 and 2023, and money always becomes part of that conversation eventually.

The math: The average cost of center-based infant care in the US is $1,230 per month. In high cost-of-living states, it exceeds $2,000. For many households, infant childcare costs more than the mortgage. Source: Economic Policy Institute, 2024.

Caregiving Changes

A Parent, a Spouse, or Your Own Health

Caregiving tends to arrive quietly and then accelerate faster than anyone expected. A parent’s health changes gradually, then all at once. A spouse receives a diagnosis. Or the health issue is yours, which adds a layer that the other scenarios do not have, because income drops and expenses increase at the same time.

The scale: 53 million Americans provide unpaid caregiving, with the average situation lasting 4.5 years. Separately, 1 in 4 working adults will experience a disability lasting 90+ days before retirement, and only 33% of private sector workers have long-term disability coverage. Source: AARP, Social Security Administration, Bureau of Labor Statistics.

Relationship Changes

Divorce or Separation

This one deserves to be named directly. Divorce is one of the most financially disruptive transitions a woman in her 30s, 40s, or 50s can go through, and it is not talked about nearly enough in practical financial terms. The income disruption is immediate. The full picture often takes 12 to 18 months to become clear.

The gap: Women’s household income drops an average of 41% in the year following divorce, compared to 23% for men. The financial recovery gap is significant and consistently underestimated. Source: US Census Bureau, Journal of Marriage and Family.

What All Financial Transitions Have in Common

Every one of these scenarios is a different path to the same financial question: What does your household actually look like on one income?

The families that navigate these transitions best are not the ones who predicted which scenario was coming. They are the ones who knew their number before they needed to use it.

4 Categories

Different life events. One financial question.

30 Minutes

What it takes for most families to calculate their household floor and get a clearer picture of their options.

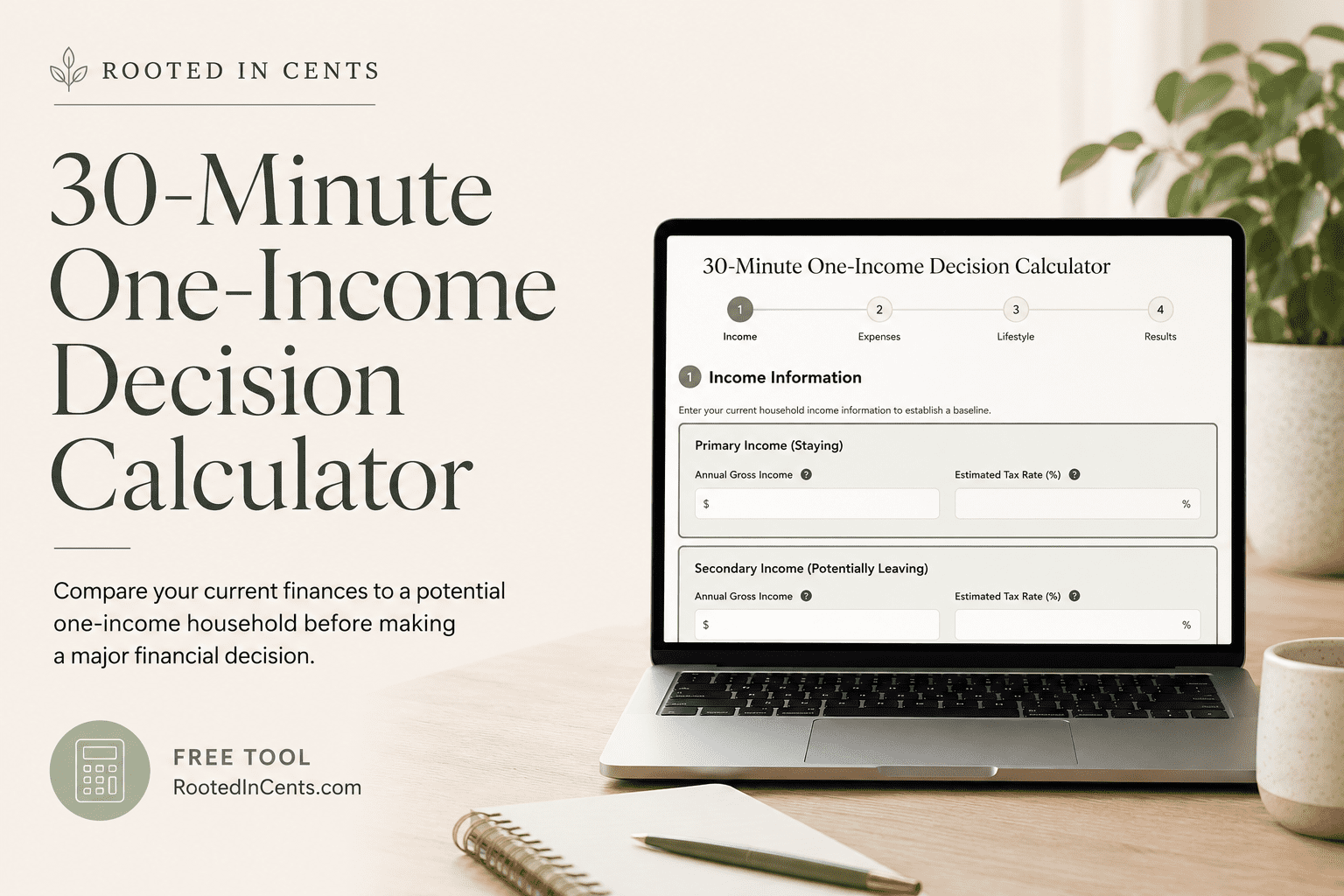

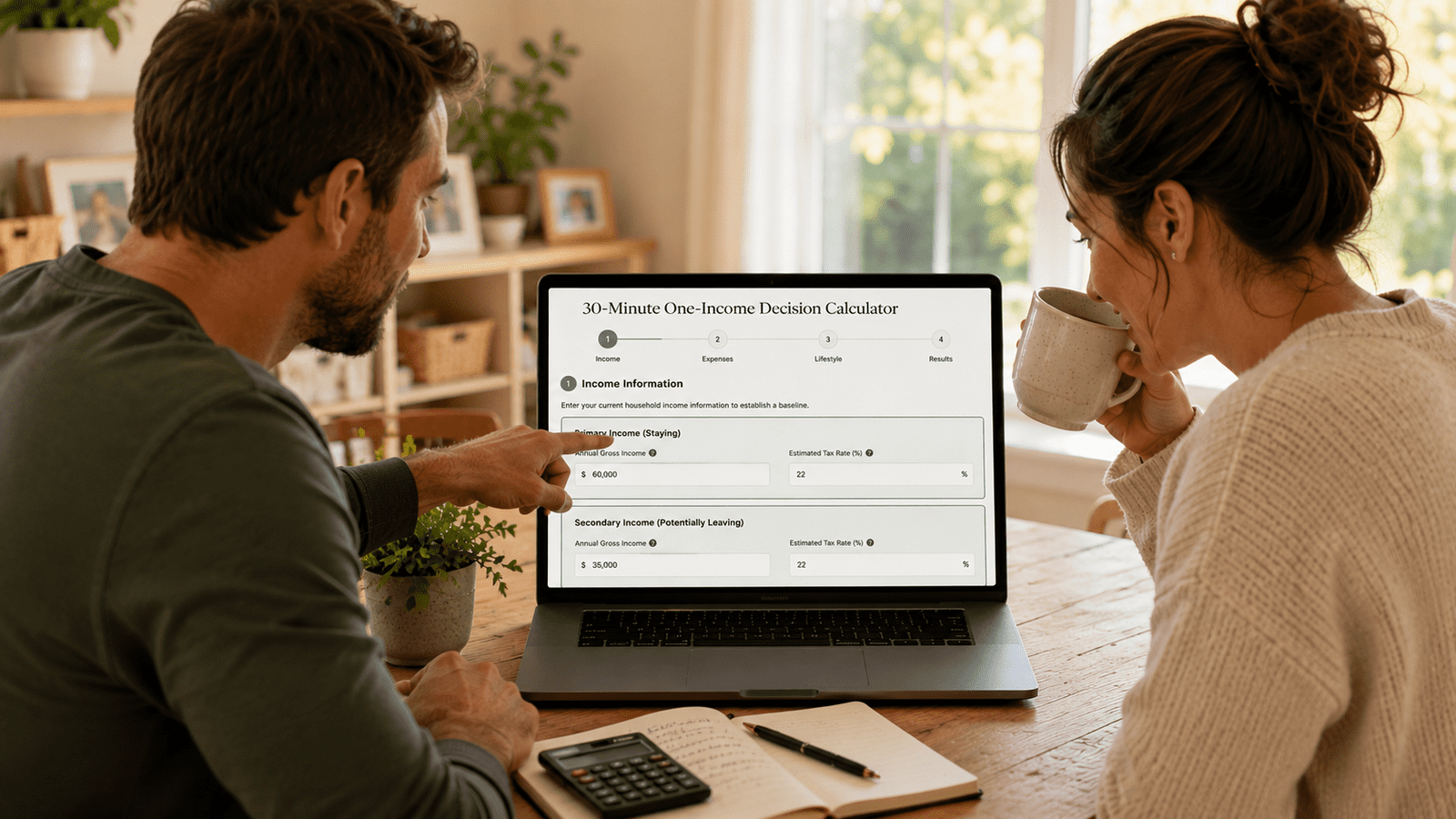

Find Out Where Your Household Actually Stands

The free 30-Minute One-Income Decision Calculator walks you through your real monthly numbers, helps you identify the minimum income your household needs each month, and shows you the gap between one income and your current expenses.

Most families can gather their numbers, work through the calculator, and have a clearer answer in about 30 minutes.

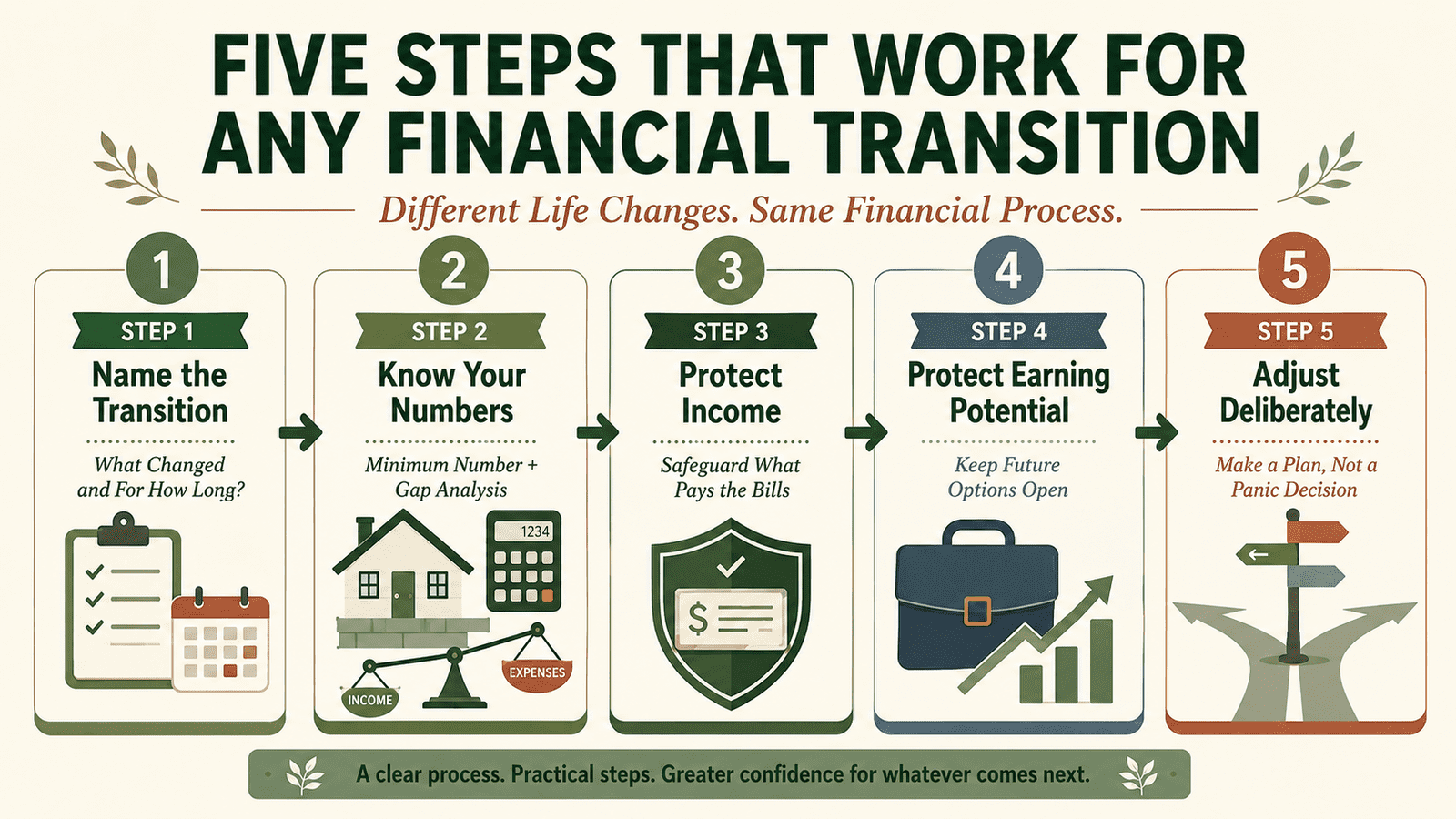

5 Steps That Work for Any One-Income Transition

STEP 1: Name the Transition

Identify what changed and how long it is likely to last. A situation that lasts three months requires a different plan than one that lasts three years. A spouse finds a new job. Maternity leave ends. A divorce, a chronic illness, a decision to homeschool.

These all have different timelines. Knowing the difference keeps you from making permanent decisions based on temporary pressure.

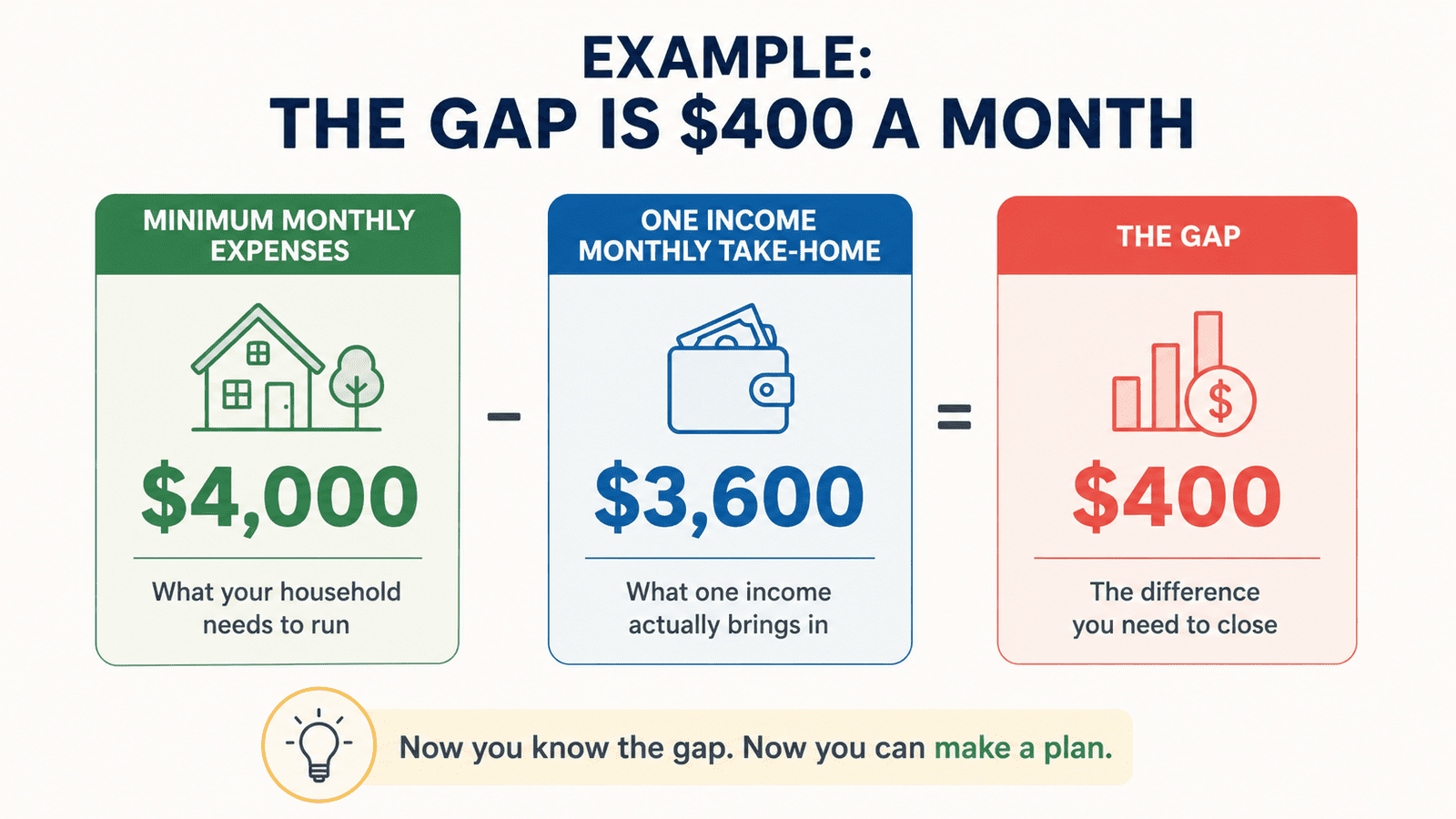

STEP 2: Know your numbers.

First, calculate your minimum number. That is the least amount of income your household needs each month to keep running. Not your current lifestyle. The essentials: housing, utilities, insurance, transportation, groceries, and minimum debt payments.

Then find the gap. The difference between that number and what one income actually brings in.

The gap may be smaller than you expected, or larger than you’d like. Either way, you cannot make a plan until you know the number. Once you know it, you can make decisions based on facts instead of fear.

STEP 3: Protect the income you have.

When a household is running on one income, that income becomes the family’s most important asset. Protect it. For us, that meant I handled the bills, schedules, and household so my husband could focus on doing his job well.

It also meant we kept saving, even if it was only $50 or $100 a month. A small emergency fund does not solve every problem, but it creates breathing room when life throws something unexpected your way.

STEP 4: Protect Income

This is the step most people skip, and it is the one that matters most for your long-term financial security. If you leave the workforce temporarily, don’t completely disconnect from it. Keep a professional relationship active.

Maintain a skill. Understand what re-entry looks like in your field. Even a small amount of consulting, freelance work, or part-time income can keep important doors open. The goal isn’t to stay fully employed. The goal is to preserve options for the future.

STEP 5: Adjust Deliberately

When income changes, lifestyle adjusts. That is not a failure. It is part of adapting to a new reality. The adjustments you make during a transition are not permanent. They are decisions that buy time and create room to think clearly.

The families that recover fastest are not the ones who cut the most aggressively. They are the ones who made a clear, intentional plan early.

Know Your Number Before You Need It

The 30-Minute One-Income Decision Calculator works for any scenario: layoff, new baby, caregiving, relocation, illness, homeschooling, or divorce. It walks through your real monthly numbers and shows you exactly where your household stands. Get the Free Calculator

One question before you go

What was the moment you realized your household’s financial picture was going change?

Share it in the comments.

Someone else reading this needs to know they are not alone in having that moment.