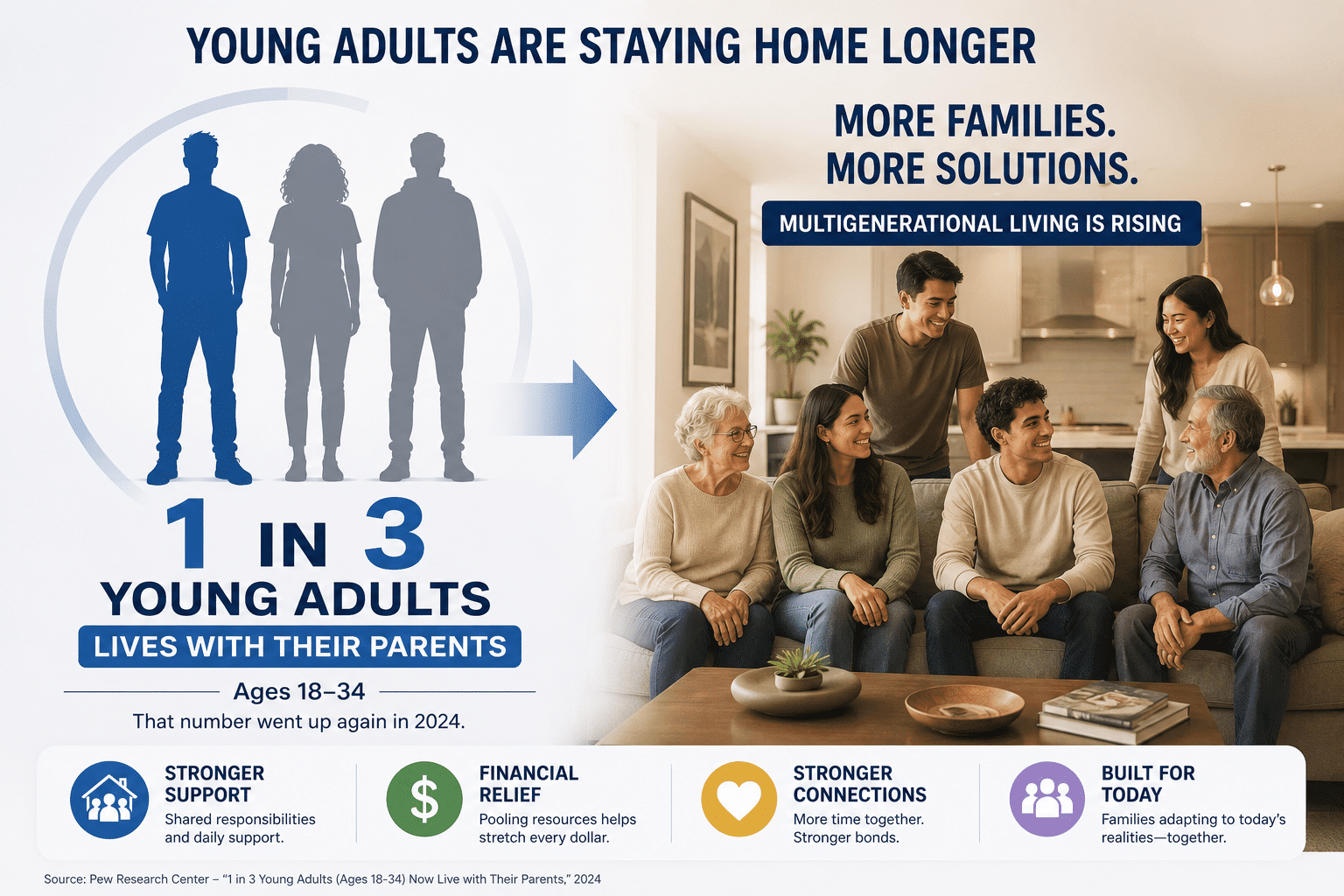

One in three young adults now lives with their parents. Multigenerational home purchases recently reached a record high. Across the country, families are quietly making financial decisions that would have seemed unusual just a generation ago.

And yet many people still talk about these changes as though they represent failure.

I think that misses what is actually happening.

Parents are helping adult children longer than they expected. Young adults are moving back home after college. Families are combining households. Some are delaying independence. Others are creating entirely new living arrangements to make the numbers work.

Not because they lack ambition. Not because they are unwilling to work. And not because they have given up on independence.

They are adapting to a financial reality that looks very different from the one many previous generations experienced.

For decades, the path seemed straightforward. Go to school. Get a job. Move out. Build a life. The assumption was that if you worked hard and made responsible choices, financial independence would naturally follow.

Today, many families are discovering that the math behind that assumption has changed.

Housing costs have risen far faster than wages. Insurance, transportation, healthcare, and everyday living expenses continue to consume a larger share of household budgets. The traditional timeline for leaving home and building an independent household has become increasingly difficult to achieve, even for young adults who are working, studying, and doing everything they were told to do.

This is not a story about laziness, entitlement, or declining work ethic.

It is a story about economic realities changing faster than many families expected.

And it is forcing people to rethink what independence, stability, and financial success actually look like.

1 in 3 young adults ages 18 to 34 now live with their parents, per the 2024 American Community Survey

17% of all U.S. home purchases in 2024 were multigenerational, a record high per NAR

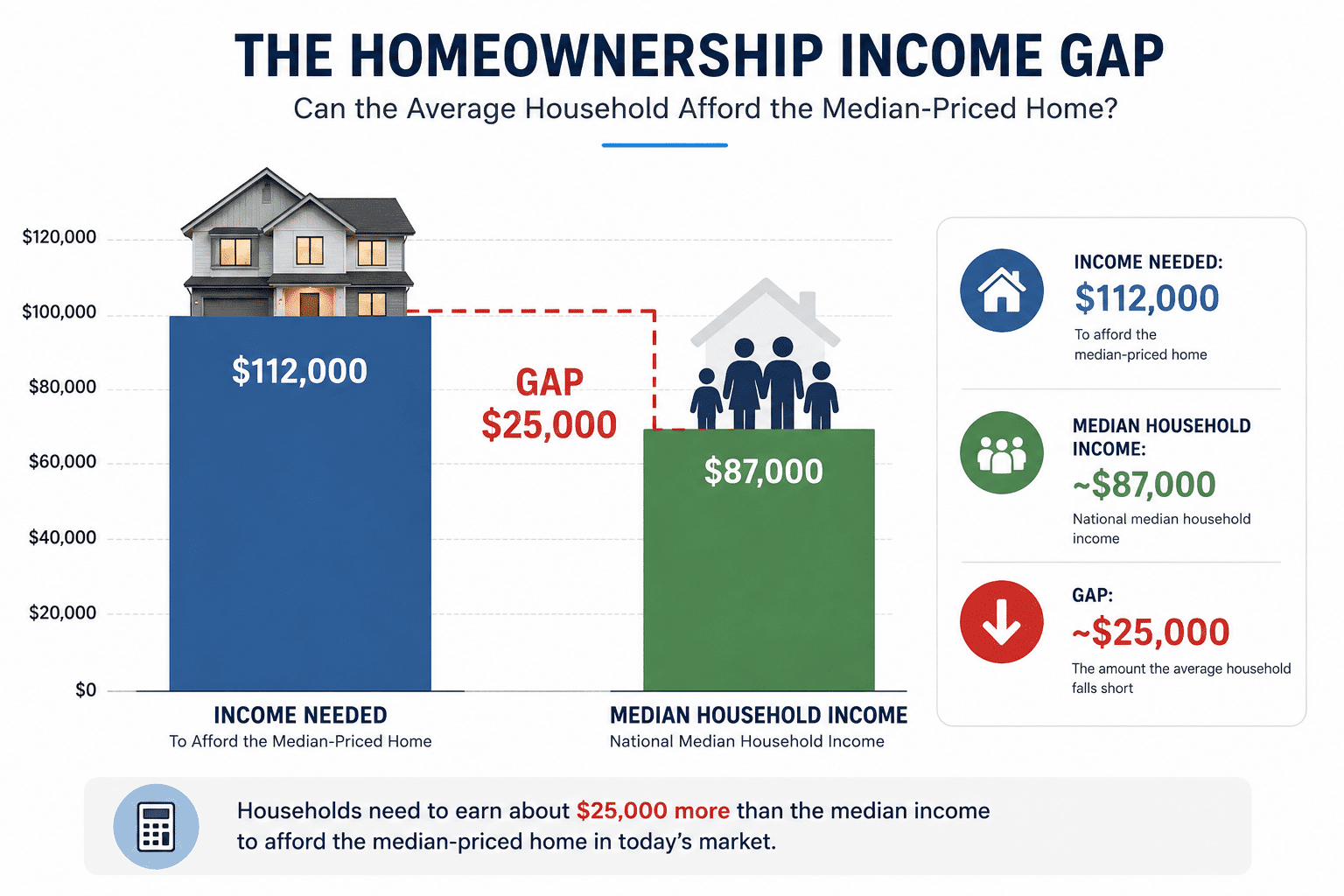

$112,000 annual income needed to afford the median-priced U.S. home,

roughly $25,000 above the median household income

1. The Reality

The Financial Math Behind Launching Into Adulthood Has Changed Dramatically

When many people in their forties and fifties look back at how they launched into adulthood, it feels reachable in a way that is hard to fully explain. Working multiple jobs still covered a small apartment. Moving to a new city was difficult but doable. Building a life from scratch was genuinely hard, but the numbers could work.

The numbers look very different now. Not slightly different. Dramatically different.

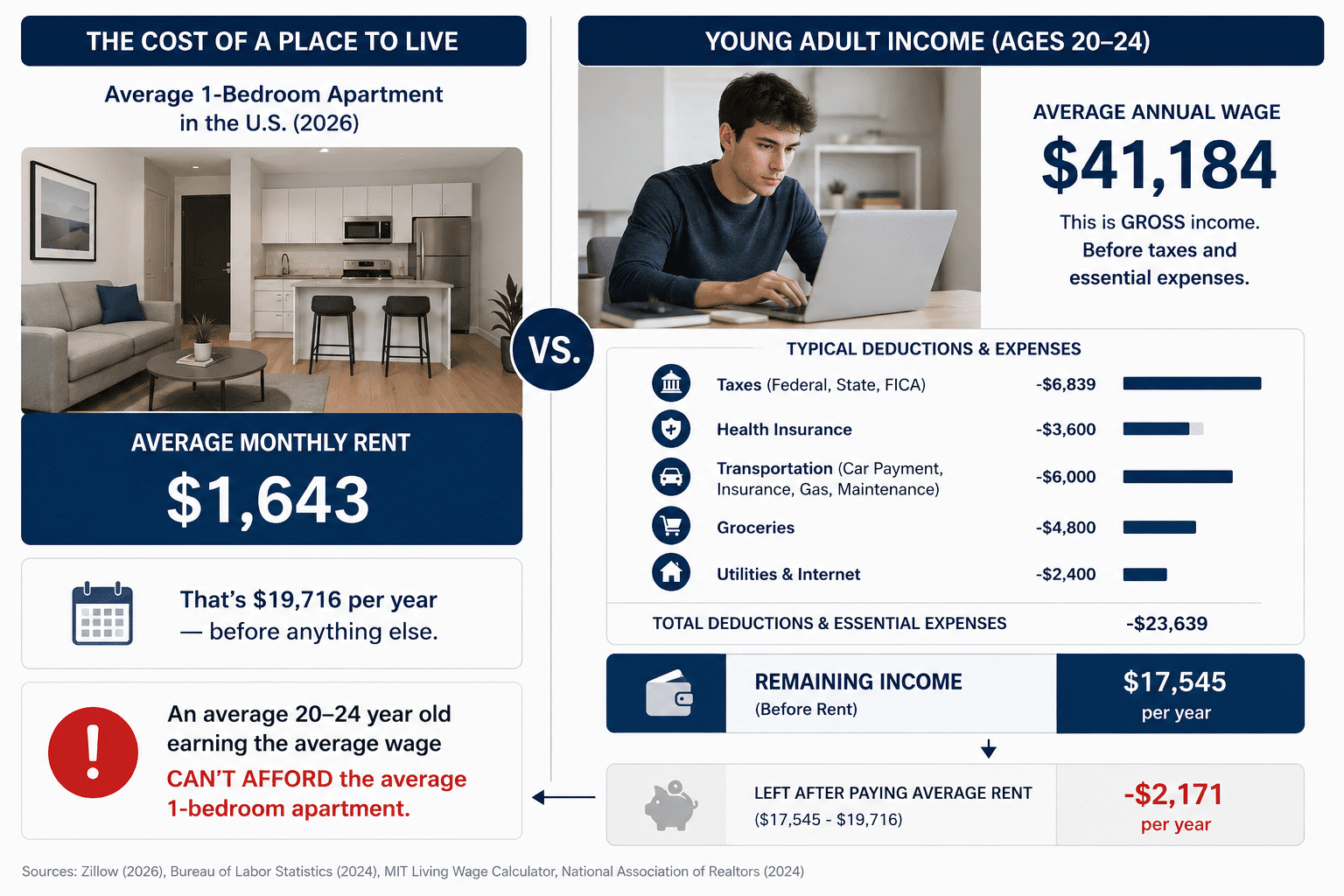

The median home price in the United States has risen roughly 90 percent in the past decade. The average one-bedroom apartment now rents for $1,643 per month nationally, according to 2026 data. The average annual wage for someone between 20 and 24 years old is $41,184. Before a single other expense, a young adult working a typical entry-level job is already spending more than 47 percent of their gross income just on rent.

The gap between wages and housing has widened sharply:

Over the past decade, urban rents have increased by roughly 4 percent per year, while wages for many full-time workers have grown much more slowly. Home prices have also outpaced income growth, making it increasingly difficult for young adults to save for a down payment while covering everyday living expenses.

A median-priced home in 1969 cost approximately five years of a young adult’s income. Today, that same benchmark is closer to nine years. The challenge is not simply that housing is expensive. The challenge is that the relationship between income and housing costs has fundamentally changed.

And housing is only part of the picture. Insurance costs have continued climbing. Transportation is expensive. Groceries have put significant pressure on household budgets. Many young adults are entering adulthood already financially stretched, carrying student debt or starting at wages that have not kept pace with the actual cost of building an independent life.

Could an eighteen-year-old today realistically do what many people did thirty years ago? In most parts of the country, the honest answer is probably not.

2. The Context

This Is Not a Story About Work Ethic. It Is a Story About Changed Systems.

Personal responsibility still matters. Work ethic still has value. Good financial habits still make a real difference in what a family is able to build over time. None of that has changed.

But there is a difference between a young adult who is not trying and a young adult who is doing many of the right things and still not gaining traction. And right now, a lot of families are dealing with the second situation more than the first.

Many young adults are putting in applications, showing up prepared, following up, and still not getting callbacks. Some are building skills and credentials as fast as they can and still finding the entry points into stable employment harder to reach than they expected. This is not a universal experience, but it is common enough that families in very different communities and circumstances are describing the same thing.

What the Data Shows

Among young adults ages 25 to 34, one in four lived in a multigenerational family household in 2021, up from just 9 percent in 1971. That is not a generational character shift. That is an economic one. The cost of simply getting started has become a significant barrier for a large portion of young adults, regardless of their work ethic or intentions.

Getting your foot in the door professionally also feels different than it did in previous generations. Local networks, industry familiarity, and existing relationships play a significant role in many hiring decisions, particularly in smaller communities. Young adults who are new to a labor market, even when they are qualified and ready to work, often face barriers that have nothing to do with their preparation or effort.

Recognizing these realities is not making excuses. It is getting an accurate picture of what families are actually navigating. And an accurate picture is the only starting point for figuring out what to do next.

3. The Shift

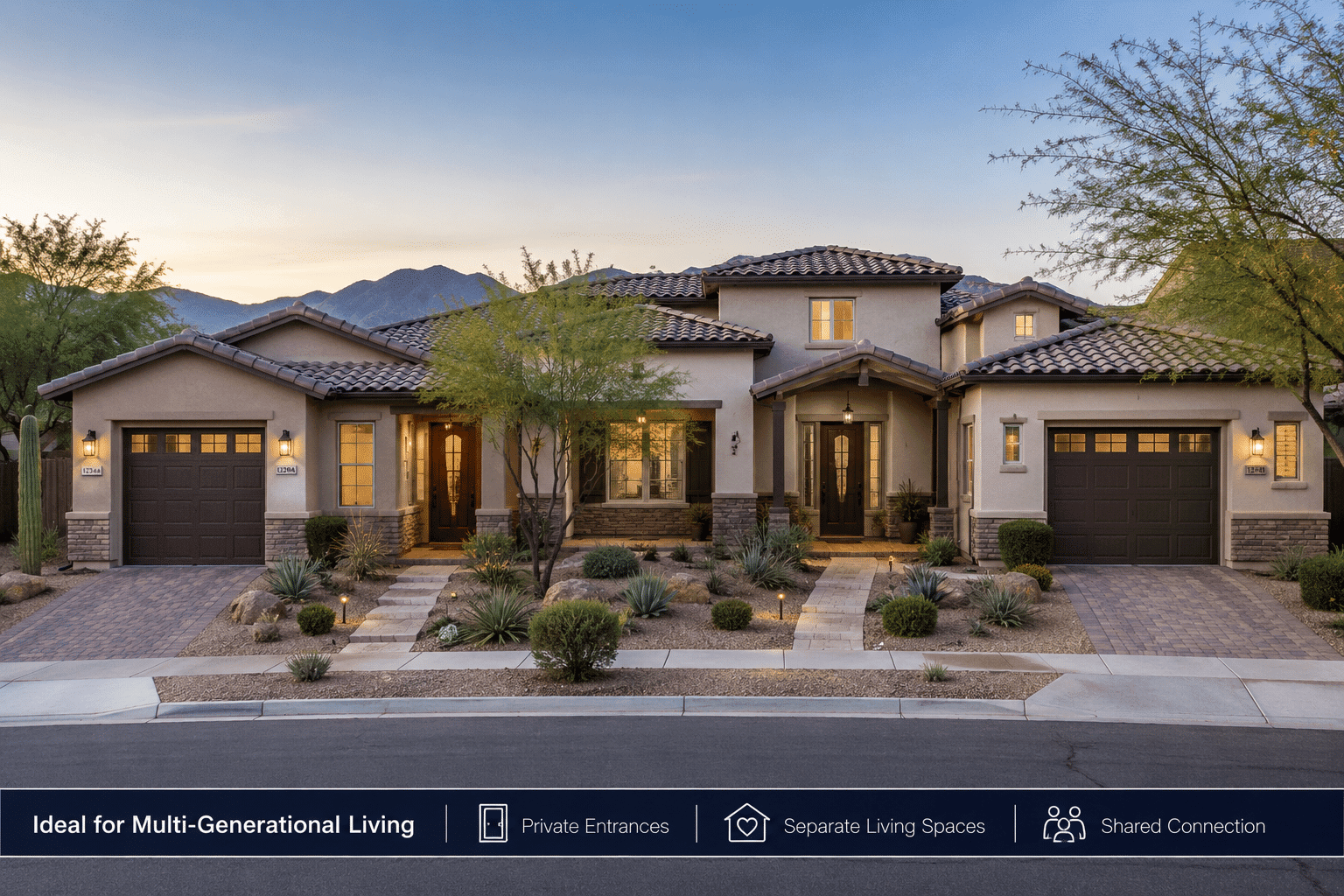

Multigenerational Living Is Becoming Normal Again, and Families Are Choosing It

For a long time, multigenerational living carried a social stigma in many American communities. It was seen as something families did only when they had no other choice. That perception is shifting, and the data reflects it.

In 2024, multigenerational home purchases hit a record high. Seventeen percent of all home purchases in the United States were multigenerational, according to the National Association of Realtors. That is a significant number. And when those buyers were asked why, 36 percent cited cost savings as the primary reason, up sharply from 15 percent in 2015.

Twenty-one percent of multigenerational buyers in 2024 mentioned adult children moving back into the home. Twenty percent said their adult children had never left. Both of those numbers have grown considerably over the past decade.

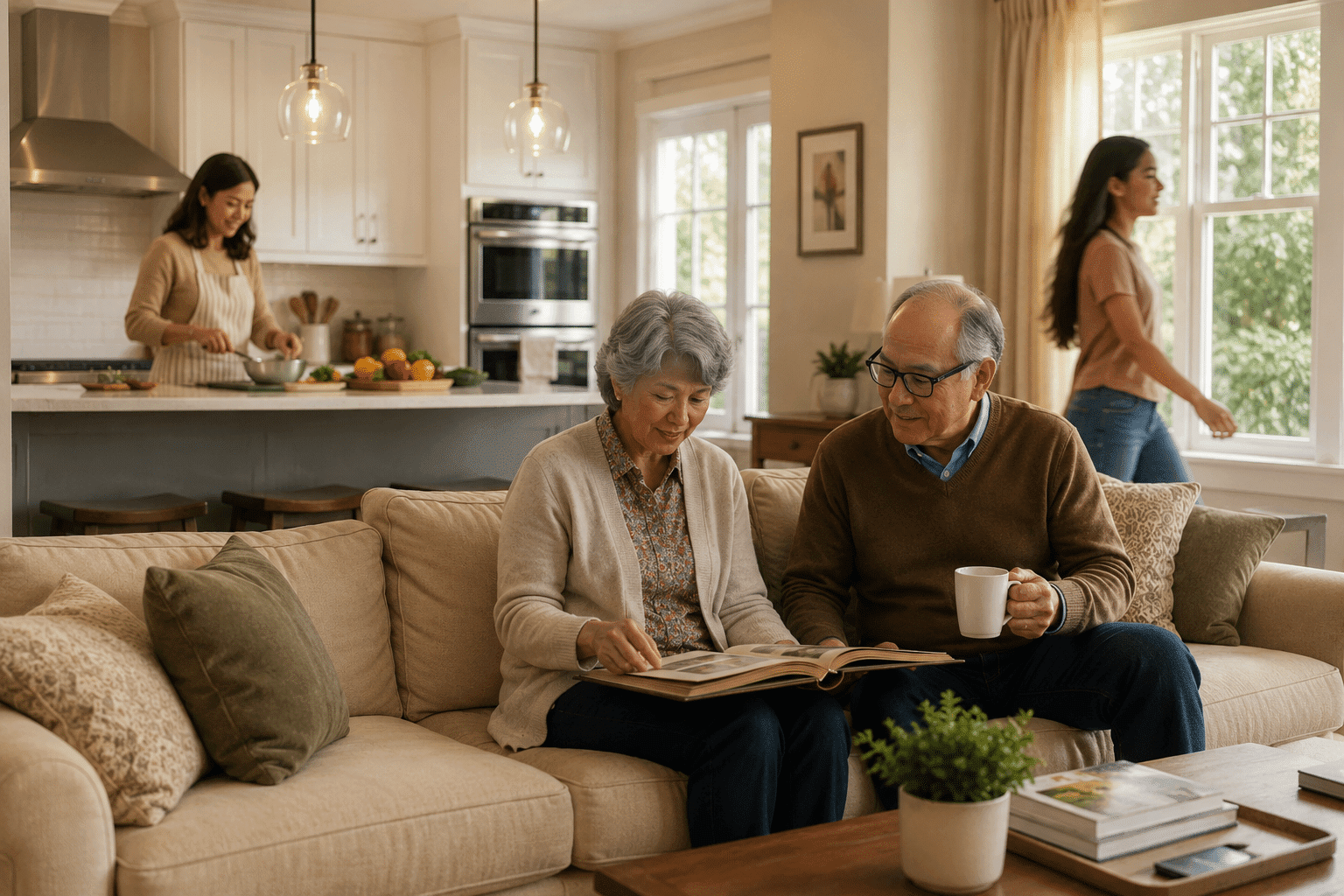

What multigenerational living actually looks like today: Many families are not simply cramming everyone into the same small space. Homes designed specifically for multigenerational living are becoming more common, with separate entrances, separate living areas, and independent spaces within the same structure. Families are purchasing properties this way intentionally, building flexibility into their housing rather than treating it as a last resort.

Roughly 59.7 million Americans, about 18 percent of the U.S. population, live in multigenerational family households, according to Pew Research Center analysis. That number quadrupled between 1971 and 2021. And among adults ages 65 and older, 22 percent now live in multigenerational arrangements, up from 17 percent in 1990. This is not a trend driven only by young adults. It is happening across generations simultaneously.

Many families are building homes and support systems that allow grandparents, parents, and adult children to share resources and space while still maintaining meaningful independence. The structure looks different from what many people grew up expecting, but the goal is the same: stability, flexibility, and the ability to take care of each other when life changes.

That is adaptation. And I think it is worth calling it what it is.

4. The Question

What Does Financial Stability Actually Look Like for Families Today?

I think many families are beginning to ask a different set of questions than the ones that defined financial success for previous generations.

Not just: how much money do we make? But: how much flexibility do we actually have if something changes?

Could one parent step back if needed?

Would the household survive a layoff without going into debt?

How would the family manage a season of caregiving for aging parents?

Do young adults have the time they need to build a stable footing before taking on financial pressure that could set them back for years?

Sometimes real financial stability is not about maximizing income. It is about creating enough breathing room to make thoughtful decisions when life changes unexpectedly.

For many families, that kind of stability means rethinking what the household structure looks like. It means making intentional decisions about housing, fixed expenses, and timelines instead of following a script that was written for a different economic environment.

It also means understanding your household’s actual financial pressure points before a crisis forces you to figure them out under pressure. Most families do not know how long they could sustain their current lifestyle if one income changed. Most families do not know exactly which expenses are fixed and which ones create real flexibility. And most families have never run the numbers on what a multigenerational or lower-cost living arrangement would actually do for their long-term stability.

That kind of clarity is more valuable than a simple income number. It is the difference between reacting to a financial transition and navigating it intentionally.

5. Practical Steps

Eight Ways Families Are Adapting to Today’s Financial Reality

These are not radical changes. They are the kinds of decisions that create real breathing room, reduce financial pressure, and help families navigate transitions more thoughtfully instead of reactively.

1. Test the one-income math before life decides for you. Job changes, caregiving responsibilities, childcare costs, military transitions, and other life events can force families to reconsider how they earn and spend money.

The 30-Minute One-Income Decision Calculator helps you compare your current financial situation to a projected one-income budget, identify potential gaps, and understand where adjustments may be needed. Instead of guessing, you’ll be able to see the numbers for yourself and make decisions from a position of clarity rather than panic.

2. Reduce fixed expenses before a crisis hits. Smaller recurring obligations create breathing room when income changes unexpectedly. Every fixed expense you carry is a commitment your household has to meet regardless of what else happens. Reviewing and reducing those obligations before something changes gives you options that will not be available during a crisis.

3. Build emergency savings gradually and consistently. Even small monthly contributions make a meaningful difference over time. The goal is not a perfect number right away. It is a habit and a direction. A household with $3,000 in savings is in a fundamentally different position when something changes than a household with nothing set aside.

4. Reduce grocery waste and food costs intentionally. Food is consistently one of the most flexible categories in a household budget, and also one of the least examined. Meal planning, cooking from what you have, and tracking your total food spending rather than just the grocery store total can free up real money without reducing quality of life.

5. Build flexibility into your housing situation. If you are in a position to choose your living situation, think about whether it supports changing family needs. Homes with separate spaces for additional family members, lower-cost regions that allow more financial breathing room, and living arrangements designed with transitions in mind are all worth considering before you need them.

6. Delay lifestyle inflation deliberately. Not every raise needs to become a larger payment or a bigger fixed obligation. The gap between what you earn and what you spend is where financial flexibility lives. Protecting that gap, especially during years when income is growing, creates options during years when it might not.

7. Build shared support systems within your family. Shared resources, combined households, and mutual support between generations reduce the financial strain on individual family members and help everyone transition more gradually into the next stage. This is not dependence. It is coordination.

8. Focus on long-term stability rather than the appearance of it. Financial peace comes from sustainable systems and intentional choices, not from looking a certain way to people around you. The families who build real stability are often the ones who made quiet, unsexy decisions over a long period of time and were not particularly concerned with whether those decisions looked impressive from the outside.

What Families Are Actually Navigating Right Now

Many families are discovering that the financial assumptions they grew up with no longer match today’s reality.

Housing costs have risen faster than incomes. Entry-level wages have struggled to keep pace with living expenses. Financial transitions that once seemed temporary are becoming longer-term decisions that require more planning and flexibility.

Families are adapting in different ways. Some are combining households. Some are delaying major financial decisions. Others are rethinking work, caregiving, retirement, or housing arrangements altogether.

The goal is not to follow someone else’s financial timeline.

The goal is to understand your options before you need them.

Understand Your Financial Flexibility Before Life Changes

Whether you’re considering a one-income household, preparing for a job transition, helping an adult child, or simply trying to create more financial breathing room, knowing where you stand today can help you make better decisions tomorrow.

The 30-Minute One-Income Decision Calculator allows you to compare your current two-income budget with a potential one-income scenario, evaluate the impact on your monthly cash flow, and identify potential gaps before making a major financial change.

A Personal Note

Years ago, I left a six-figure career to stay home and raise our boys. We adjusted our lifestyle, navigated military transitions, and built a life that gave our family more flexibility when circumstances changed.

That experience taught me something important: financial stability is rarely about predicting every change. It is about creating enough margin and flexibility to adapt when change inevitably comes.

That is the purpose behind Rooted in Cents. Helping families understand their options, run the numbers, and navigate financial transitions with greater confidence.

Sources: 2024 American Community Survey / NAHB (November 2025), National Association of Realtors 2025 Generational Trends Report, Pew Research Center Multigenerational Living Analysis, Zillow 2026 Rental Data, BLS Occupational Employment and Wage Statistics 2025, Harvard Joint Center for Housing Studies 2025