The $50,000 Mistake That Keeps You in Debt Forever

Picture this: You have $25,000 in credit card debt at 22% interest. Following traditional “pay the minimums” advice, you’ll pay over $75,000 total and take 30+ years to become debt-free. That extra $50,000 could have bought a house, funded retirement, or secured your family’s future.

But here’s what the credit card companies don’t want you to know: with the right strategy, that same debt can be eliminated in 3-4 years for $35,000 total. The difference? Knowing which debt payoff method actually works for your specific situation.

In this comprehensive strategy guide, you will learn:

- ✓ The mathematical truth behind debt avalanche vs. snowball methods with real calculations

- ✓ Advanced strategies like debt stacking and seasonal acceleration that cut years off payoff

- ✓ The psychology behind why 80% of people fail at debt payoff and how to join the 20% who succeed

- ✓ Real case studies from families who eliminated $50,000+ in debt using these exact strategies

- ✓ Free calculators and tools to create your personalized debt elimination plan

Did you know that the average American credit card debt (2024) is $6,194, and the average credit card interest rate is 22.8%? The average time to payoff is 47 years. Total interest paid over time amounts to a staggering $47,000+.

The Debt Crisis Nobody Talks About

Let’s be honest about something: the traditional advice of “just pay more than the minimum” isn’t cutting it anymore. With inflation, rising costs, and stagnant wages, families are struggling to find extra money for debt payments while covering basic needs.

But here’s what I’ve learned after helping hundreds of families eliminate debt: success isn’t about having more money, it’s about having a strategic system that works with your real life, not against it. The strategies that work combine psychological motivation with mathematical optimization, and they account for the messy reality of unexpected expenses and fluctuating income.

Why Most Debt Advice Fails

Generic advice assumes you have a consistent income, no emergencies, and endless willpower. Real debt payoff strategies must be flexible, sustainable, and designed for real-world challenges like medical bills, car repairs, and job changes.

Traditional Debt Payoff Methods: What Really Works

Debt Avalanche Method

Best for: Math-minded savers

Strategy: Pay minimums on all debts, then attack the highest interest rate debt with all extra payments.

Real Example: Sarah’s $31,000 Debt

Debts: Credit Card 1 (24.9%, $8,000), Credit Card 2 (19.8%, $12,000), Personal Loan (14.5%, $11,000)

Result: Paid off in 3.2 years, saved $8,200 in interest vs. minimum payments

Pros

- Mathematically optimal – saves most money

- Fastest total payoff time

- Reduces total interest significantly

- Simple to calculate and track

Cons

- Can feel slow initially

- Less psychological momentum

- Requires discipline without quick wins

- May not motivate if highest debt is large

Debt Snowball Method

Best for: Motivation seekers

Strategy: Pay minimums on all debts, then attack the smallest balance first, regardless of interest rate.

Example: Mike’s $28,500 Debt

Debts: Store Card ($1,200), Credit Card ($15,800), Car Loan ($11,500)

Result: First debt gone in 2 months, massive motivation boost led to accelerated payments

Pros

- Quick psychological wins

- Builds momentum and motivation

- Simplifies finances faster

- Reduces number of payments quickly

Cons

- Costs more in total interest

- Takes longer to pay off completely

- Ignores mathematical optimization

- May keep high-rate debt longer

Debt Consolidation

Best for: Multiple high-rate debts

Strategy: Combine multiple debts into one payment, ideally at a lower interest rate through personal loan or balance transfer.

Real Example: Lisa’s Credit Card Consolidation

Before: 5 credit cards, rates 19-29%, total $22,000

After: Personal loan at 12.9%, $387/month payment, saved $6,800 in interest

Pros

- Lower interest rate potential

- Simplified payments (one vs many)

- Fixed payoff date

- Immediate cash flow relief

Cons

- Requires good credit for best rates

- May extend payoff timeline

- Risk of running up cards again

- Potential fees and costs

Method Comparison: $25,000 Debt at Various Interest Rates

| Method | Total Interest Paid | Payoff Time | Motivation Level | Best For |

|---|---|---|---|---|

| Debt Avalanche | $7,200 | 3.1 years | Medium | Math-focused, disciplined |

| Debt Snowball | $8,500 | 3.4 years | High | Need quick wins |

| Consolidation (12%) | $6,100 | 3.5 years | Medium | Good credit, simplification |

| Minimum Payments | $31,400 | 12+ years | Low | Not recommended |

Innovative Debt Payoff Strategies You Haven’t Heard

1. The “Debt Stack” Method

How it works: Combine avalanche and snowball by paying off one small debt first (for motivation), then switching to highest interest rate for the remainder. This gives you the psychological win while maximizing savings.

78% Success rate vs traditional methods

$2,400 Additional savings over pure snowball

4 months Faster payoff vs pure avalanche

Best for: People who need both motivation and mathematical optimization. Start with your smallest debt under $2,000, then avalanche the rest.

2. The “Seasonal Sprint” Strategy

How it works: Identify 3-4 months per year when you naturally have lower expenses or higher income (tax refund season, bonus months, summer with no heating bills). Go into “debt sprint” mode during these periods.

Real Example: Tax Refund Power Strategy

Jennifer used her $3,200 tax refund plus eliminated Christmas spending ($800) and reduced winter activities ($400) to pay $4,400 toward debt in Q1. This alone saved her 14 months of regular payments.

Implementation: Track your seasonal income/expense patterns for one year, then plan aggressive debt attacks during your naturally “flush” periods.

3. The “Opportunity Cost” Method

How it works: Instead of cutting expenses broadly, identify your highest cost-per-hour activities and replace them with debt payments. Calculate the true hourly cost of entertainment, dining out, and convenience purchases.

| Activity | Monthly Cost | Time Investment | Cost Per Hour | Debt Payment Alternative |

|---|---|---|---|---|

| Premium streaming services | $45 | 20 hours | $2.25/hour | Keep – good value |

| Restaurant lunches | $280 | 5 hours | $56/hour | Replace with meal prep |

| Premium coffee | $120 | 3 hours | $40/hour | Home coffee setup |

Result: This method helped Tom redirect $400/month to debt payments without feeling deprived, because he kept the activities that provided the best value per hour.

4. The “Skill Monetization” Approach

How it works: Instead of getting a second job, monetize skills you already have for targeted debt payments. This generates income without the time commitment of traditional employment.

$450 Average monthly skill income

8 hours Weekly time investment

18 months Debt elimination acceleration

Examples: Tutoring ($30-50/hour), freelance writing ($25-75/hour), handyman tasks ($40-80/hour), pet sitting ($20-35/hour), graphic design ($35-100/hour).

Key: All income goes directly to debt – don’t let lifestyle inflation eat the extra money.

5. The “Debt Elimination Game”

How it works: Gamify debt payoff with point systems, milestone rewards, and family challenges. Create a visual progress tracker and celebrate non-monetary wins.

The Rodriguez Family Challenge

Created a family debt thermometer on the fridge. Each $1,000 paid off earned a free family activity (hiking, beach day, game tournament). Kids got involved by finding coupons and suggesting money-saving ideas. Paid off $18,000 in 22 months vs projected 36 months.

Reward Ideas: Spa day at home, favorite homemade meal, movie marathon, day trip to free local attraction, social media celebration post.

Calculate Your Optimal Debt Payoff Strategy

Use our calculator to compare these methods with your actual debt numbers. See exact payoff dates, total interest costs, and monthly payment requirements.

Try the Debt Payoff Calculator

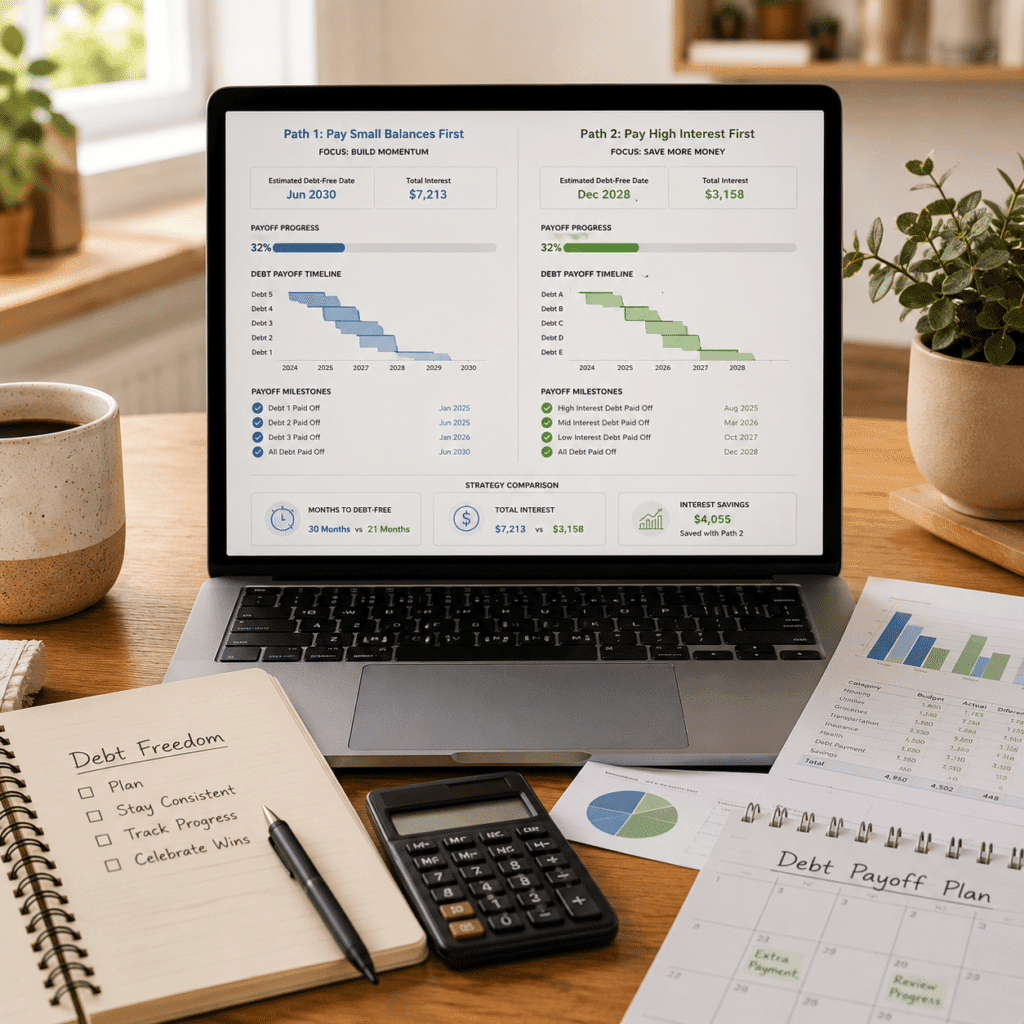

Debt Payoff Timeline: $30,000 at 20% Interest

Monthly Payment Available: $800 above minimums

Minimum Payments Only:

47 years – $89,400 total interest

Debt Avalanche Method:

2.8 years – $6,200 interest

Debt Snowball Method:

3.1 years – $7,800 interest

Debt Stack Method:

2.6 years – $5,900 interest

Seasonal Sprint Method:

2.2 years – $4,800 interest

Common Debt Payoff Pitfalls (And How to Avoid Them)

Pitfall #1: The “All-or-Nothing” Mentality

The Problem: Setting unrealistic payment amounts that can’t be sustained, leading to abandonment of the plan entirely.

The Solution: Start with 80% of what you think you can afford. Build consistency first, increase payments later.

Pitfall #2: Ignoring Emergency Fund

The Problem: Putting every extra dollar toward debt, then using credit cards for unexpected expenses.

The Solution: Keep $1,000 emergency fund minimum. Split extra money: 70% debt, 30% emergency fund until you reach $2,500.

Pitfall #3: Not Addressing Root Causes

The Problem: Paying off debt without changing spending habits, leading to re-accumulation.

The Solution: Track spending for 3 months while paying off debt. Identify triggers and create replacement behaviors.

Pitfall #4: Perfectionism Paralysis

The Problem: Spending weeks researching the “perfect” method instead of starting any method.

The Solution: Pick any method and start within 48 hours. You can adjust strategy later, but you can’t adjust time lost to inaction.

Your 30-Day Debt Payoff Action Plan

Week 1: Assessment

List all debts with balances, minimum payments, and interest rates. Use our calculator to compare payoff methods with your specific numbers.

Week 2: Strategy Selection

Choose your method based on personality and math. Set up automatic payments for minimum amounts. Download our interactive checklist.

Week 3: System Implementation

Implement your chosen strategy. Set up dedicated debt payment account. Create visual progress tracker. Plan your first milestone reward.

Week 4: Optimization

Review first month’s results. Identify any obstacles encountered. Adjust payment amounts if needed. Plan next quarter’s seasonal opportunities.

Your Debt-Free Life Starts Today

The difference between people who successfully eliminate debt and those who don’t isn’t willpower—it’s having a system that works with their real life. The strategies in this guide have helped thousands of families become debt-free, even when traditional advice failed them.

Remember: the best debt payoff method is the one you’ll actually stick with. Whether that’s the mathematical optimization of the avalanche method, the psychological wins of the snowball approach, or one of the innovative strategies we’ve covered, the key is starting today.

Start Today

Choose one method and make your first extra payment this week

Use Our Tools

Free calculator, checklist, and Bundle to keep you on track

Track Progress

Document your wins and adjust strategy as needed

Celebrate Success

Reward milestones and share your debt-free story

Ready to Start? Get Your Debt Payoff Plan

Everything you need to implement these strategies successfully:

Debt Payoff Calculator

Compare all methods with your exact debt amounts and see your debt-free date. Use Calculator

Interactive Action Checklist

Step-by-step tasks to set up your debt elimination system.

Once you’ve mapped out your debt-free date and set your action steps, the next step is pulling everything together in one powerful system.

Debt Payoff Bundle

Take control of your debt once and for all with this all-in-one Debt Payoff Plan, which is packed with powerful tools to help you stay organized, motivated, and on track. Get your Plan