50 Proven Ways to Save Thousands without Feeling Deprived

Here’s the frugal living truth nobody talks about: Smart families save $3,000-$10,000+ annually through strategic choices that actually improve their quality of life. This isn’t about extreme couponing or living in deprivation—it’s about maximizing value from every dollar you spend.

Real frugal living means making intentional decisions about housing, transportation, and daily expenses that compound into massive savings while maintaining comfort and enjoyment. The goal isn’t spending less—it’s spending wisely on what truly matters.

In this comprehensive frugal living guide, you will learn:

- ✓ The Big Three strategies that save $3,000-$10,000+ annually

- ✓ Housing optimization tactics that cut costs without downsizing lifestyle

- ✓ Transportation strategies that save hundreds monthly

- ✓ Smart shopping and entertainment alternatives that maintain quality

- ✓ Advanced money-saving tactics for experienced frugal livers

Tired of living paycheck to paycheck but worried that “being frugal” means giving up everything you enjoy? Here’s how to save serious money while actually improving your quality of life.

You’re tired of the financial stress, but every piece of money advice feels like it’s asking you to live like a monk. Cut your coffee, never eat out, drive a beater car forever, and somehow be happy about it. That’s not frugal living; that’s deprivation, and it doesn’t work in the long term.

The families who master frugal living aren’t the ones who reuse money tea bags. They’re the ones who understand that small, strategic changes compound into thousands of dollars, as those who clip every coupon and reuse redirect money toward goals that actually matter.

Why Your Current Money-Saving Attempts Are Failing

Before we dive into what works, let’s talk about why most people’s frugality attempts fizzle out within a few months.

The Deprivation Trap

You start strong, cutting every possible expense. No coffee shops, no takeout, no entertainment, no new clothes. For a few weeks, you feel virtuous watching your bank account grow. Then life happens: a stressful week at work, a friend’s birthday, a sale on something you’ve been wanting, and you “blow” your budget.

The problem? You set yourself up for failure by trying to change everything at once and cutting expenses that actually brought you joy or convenience.

The Penny-Wise, Pound-Foolish Problem

You spend an hour driving across town to save $3 on groceries, but you haven’t looked at your insurance rates in three years. You use coupons religiously but never negotiate your salary. You’re focused on saving coins while dollars walk out the door.

The All-or-Nothing Mindset

Frugal living isn’t a binary choice between spending freely and living like it’s the Great Depression. It’s about making conscious trade-offs. Maybe you spend money on high-quality coffee beans to brew at home instead of buying coffee shop drinks. Maybe you buy premium ingredients to make restaurant-quality meals at home.

The goal isn’t to spend as little as possible; it’s to spend wisely on what matters most to you.

The Frugal Living Hierarchy: Start Where It Matters Most

Not all money-saving strategies are created equal. Some save you $20 annually, while others save you $2,000. Smart, frugal living starts with the big wins.

Level 1: The Big Three (Save $3,000-$10,000+ Annually)

Housing Optimization

Housing typically represents 25-35% of your budget, making it your biggest opportunity for savings.

- House hacking: Rent out a room, basement, or garage space for $400-800 monthly extra income

- Strategic downsizing: A home that’s 200 square feet smaller can save $200-400 monthly in mortgage, taxes, and utilities

- Location arbitrage: Living 15-20 minutes further from city centers often cuts housing costs by 20-30%

- Refinancing and shopping insurance: Even small rate improvements save hundreds annually

Transportation Revolution

Transportation is most families’ second-largest expense, but it’s also where you can make dramatic improvements:

- The reliable used car strategy: Buy 3- to 5-year-old vehicles with good reliability records. Let someone else absorb the depreciation

- One-car living: If possible in your area, sharing one reliable vehicle saves $400-600 monthly in payments, insurance, and maintenance

- Bike commuting: Even 2-3 days per week saves gas and reduces wear on your vehicle

- Strategic car buying: Research reliability ratings, buy at the right time of year, and negotiate based on actual market values

Insurance Audit and Optimization

Most families are overpaying for insurance by $1,000 to $ 3,000 annually.

- Bundle discounts: Often save 15-25% on home and auto insurance

- Higher deductibles: Raising deductibles from $500 to $1,000 can cut premiums significantly

- Annual shopping: Insurance rates change constantly. Shop every year, not every decade

- Eliminate unnecessary coverage: Do you really need roadside assistance if you have AAA?

Level 2: Daily Life Optimization (Save $1,500-$3,000 Annually)

Food Strategy Revolution

Food offers the best balance of significant savings potential with lifestyle improvement.

- Meal planning mastery: Plan meals around sales and seasonal produce. This alone saves most families $150-300 monthly

- Batch cooking and freezing: Cook large quantities when ingredients are cheap, portion, and freeze for busy weeks

- Strategic restaurant replacement: Instead of cutting dining out completely, master 3-4 restaurant copycat recipes for home

- Seasonal eating: Build your meal plans around what’s naturally in season and abundant

Subscription and Service Audit

The average household has 12 or more recurring subscriptions, spending $200–$400 monthly on services they barely use.

- The streaming shuffle: Instead of paying for 4 streaming services year-round, rotate through them seasonally

- Gym membership alternatives: Many people pay $50-100 monthly for gyms they rarely use. Consider home workouts, running, or pay-per-visit options

- Phone plan optimization: Family plans and low-cost carriers can cut phone bills by 50-70%

- Software subscription review: How many productivity apps are you paying for but not using?

Level 3: Smart Shopping and Lifestyle Tweaks (Save $500-$1,500 Annually)

These strategies require more time and attention but add up to meaningful savings:

- Strategic thrift shopping: Focus on quality items like wool coats, leather goods, and solid wood furniture

- Generic brand testing: Try store brands for basics like flour, sugar, and cleaning supplies

- Energy efficiency improvements: Programmable thermostats, LED bulbs, and weather stripping pay for themselves quickly

- DIY personal care: Basic manicures, simple haircuts, and homemade skincare can save $100+ monthly

The Psychology of Sustainable Frugality

The difference between successful long-term frugal living and short-term deprivation comes down to mindset and strategy.

Reframe Frugality as Optimization

Instead of thinking, “I can’t afford this,” ask, “Is this the best use of my money?” This shift from scarcity to strategy changes everything.

When you see a $150 dinner out, instead of feeling deprived that you “can’t” afford it, you think, “I could spend $150 on this meal, or I could use that money toward our vacation fund and make an amazing dinner at home for $30.”

Build in Planned “Splurges”

Successful frugal living includes intentional spending on things that matter to you. Maybe you:

- Buy organic produce, but shop at discount stores for household items

- Drive an older car but splurge on quality tools for your hobby

- Cook most meals at home, but budget for one nice restaurant meal monthly

- Buy most clothes secondhand, but invest in good shoes and coats

The key is making these choices consciously rather than spending impulsively.

Focus on Value, Not Just Price

Frugal living often means spending more upfront for better long-term value.

- Quality tools that last decades instead of cheap ones that break annually

- Well-made clothing that looks good for years instead of fast fashion

- A reliable used car instead of the cheapest option that needs constant repairs

- Energy-efficient appliances that save money on utilities

Advanced Frugal Living Strategies

Once you’ve mastered the basics, these advanced strategies can amplify your savings without adding complexity to your life.

The Substitution Game

Instead of eliminating expenses, find cheaper ways to get the same benefits:

- Entertainment substitutions: Museum free days instead of movie tickets, potluck dinner parties instead of restaurant outings

- Exercise substitutions: Hiking instead of gym memberships, YouTube workouts instead of personal trainers

- Learning substitutions: Library books and online courses instead of expensive workshops

- Experience substitutions: Camping instead of hotels, local adventures instead of expensive vacations

The Batch Strategy

Group similar activities together to save time and money:

- Batch errands: One trip that hits multiple stores saves gas and time

- Batch cooking: Prepare multiple meals when you’re already cooking

- Batch shopping: Stock up during sales instead of paying full price weekly

- Batch maintenance: Schedule all car maintenance, home repairs, and health appointments together

The Timing Advantage

When you buy matters as much as what you buy:

- Seasonal shopping: Buy winter clothes in spring and summer items in fall

- Holiday timing: Christmas decorations in January, candy after holidays

- End-of-model-year deals: Cars, appliances, and electronics often go on deep discount

- Bulk buying during sales: Stock up on non-perishables when they’re 40-50% off

Frugal Living for Every Life Stage

Your frugal living strategy should evolve as your life circumstances change.

Young Adults and New Graduates

Focus areas: Building habits, avoiding lifestyle inflation, maximizing learning

- House-sit, pet-sit, or rent rooms to minimize housing costs

- Invest in skills and education that increase earning potential

- Buy quality basics that will last through multiple life transitions

- Learn to cook, basic car maintenance, and other life skills

Families with Young Children

Focus areas: Managing increased expenses, time efficiency, long-term planning

- Master bulk cooking and freezer meals for busy weeknights

- Create toy and clothing swaps with other families

- Focus on free and low-cost family activities

- Buy quality children’s items secondhand (they outgrow everything quickly)

Empty Nesters and Pre-Retirees

Focus areas: Downsizing, optimizing for retirement, maintaining social connections

- Rightsize your housing for your current needs

- Travel strategically using senior discounts and off-peak timing

- Put more value on experiences and relationships than on things.

- Share resources with friends (tools, equipment, bulk buying)

Making a Plan for Living Frugally That Works for You

Living frugally well doesn’t mean duplicating someone else’s plan. It means making a plan that fits your values, way of life, and ambitions.

Step 1: An audit of spending based on values

Look at what you’ve spent in the last three months and sort it into groups:

Spending that is in line with money spent on things that are really important to you

- Convenience spending refers to money spent to save time or effort.

- Impulse spending: Money spent without conscious decision-making

- Social spending: Money spent to fit in or meet others’ expectations

Your frugal living plan should preserve aligned spending, evaluate convenience spending for value, eliminate most impulse spending, and thoughtfully reduce social spending.

Step 2: Choose Your Top 5 Focus Areas

Don’t try to optimize everything at once. Pick the five areas where you can make the biggest impact with the least disruption to your life:

- Housing costs

- Transportation expenses

- Food and dining

- Insurance and subscriptions

- Entertainment and recreation

- Clothing and personal care

- Utilities and household expenses

Step 3: Set Specific, Measurable Goals

Instead of “spend less on food,” set goals like

- “Reduce monthly grocery spending from $800 to $600 by meal planning and strategic shopping.”

- “Cut subscription costs from $180 to $80 monthly by canceling unused services.”

- “Save $200 monthly on transportation by biking to work 3 days per week.”

Step 4: Track Your Wins

Keep a simple log of money-saving victories:

- Amount saved each month in your focus areas

- Successful substitutions and alternatives you’ve discovered

- Quality of life improvements from your frugal choices

- Progress toward larger financial goals enabled by your savings

Common Frugal Living Mistakes (And How to Avoid Them)

Learning from others’ mistakes helps you avoid common pitfalls that derail frugal living efforts.

The Time-Money Confusion

Mistake: spending hours saving small amounts while ignoring bigger opportunities.

Solution: Calculate your “savings hourly rate.” If you spend 2 hours driving to different stores to save $10, you’re earning $5/hour for your time. Focus on savings strategies that give you better returns on time invested.

The Quality Compromise

Mistake: Buying cheap items that break quickly instead of quality items that last.

Solution: Research cost-per-use for major purchases. A $200 coat worn 100 times costs $2 per wear. A $50 coat that lasts 20 wears costs $2.50 per wear.

The Social Isolation Trap

Mistake: Avoiding all social activities that cost money, leading to isolation and relationship strain.

Solution: Budget for social activities and suggest cost-effective alternatives. Host potluck dinners, organize hiking groups, or suggest coffee dates instead of expensive restaurants.

The Perfectionism Problem

Mistake: Giving up entirely when you “break” your budget or make non-frugal choices.

Solution: Treat frugal living like healthy eating, one indulgent meal doesn’t ruin your diet, and one splurge purchase doesn’t ruin your budget. Get back on track with the next spending decision.

The Technology Tools That Make Frugal Living Easier

Smart use of technology can automate many frugal living strategies, saving you time while maximizing savings.

Money-Saving Apps and Tools

- Price comparison apps: Honey, Rakuten, and InvisibleHand automatically find coupon codes and better prices

- Cashback credit cards: Earn 1-5% on purchases you’re already making

- Grocery apps: Ibotta, Checkout51, and store apps provide automatic rebates

- Bill negotiation services: Truebill and Trim can negotiate lower rates on your behalf

Automation Strategies

- Automatic savings transfers: Pay yourself first by automating transfers to savings

- Bill pay automation: Avoid late fees and take advantage of autopay discounts

- Investment automation: Dollar-cost average into low-cost index funds

- Budget tracking automation: Use apps that categorize expenses automatically

Turning Frugal Living Into Wealth Building

The ultimate goal of frugal living isn’t just to spend less, it’s to redirect that money toward building real wealth.

The Savings Cascade Strategy

As you reduce expenses in one area, immediately redirect those savings toward wealth-building goals:

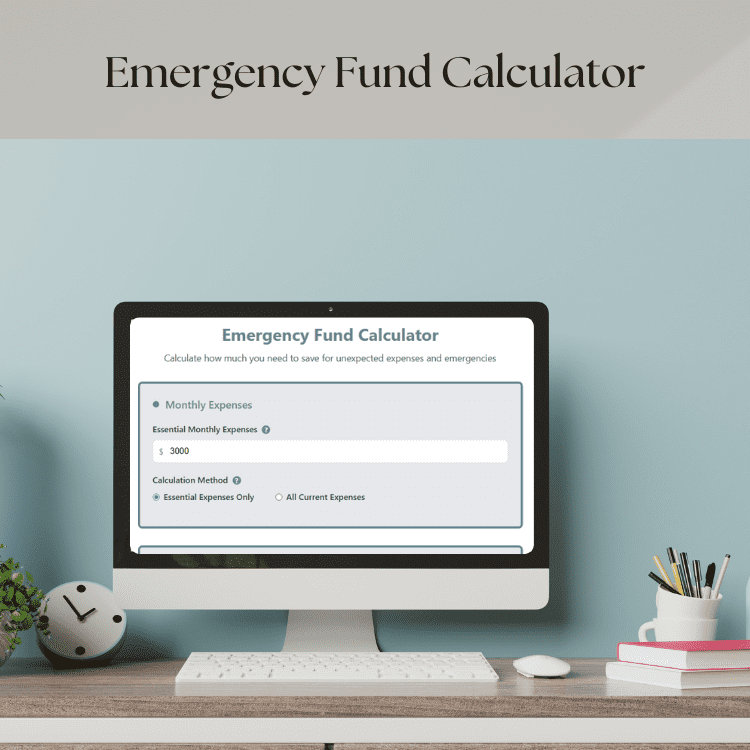

- Emergency fund: Build to $1,000, then 3-6 months of expenses

- Use our Emergency Fund Calculator to find your personalized savings target.

- High-interest debt elimination: Pay off credit cards and personal loans

- Try our Debt Payoff Calculator to compare snowball vs. avalanche strategies.

- Retirement contributions: At least enough to get employer match

- Investment accounts: Low-cost index funds for long-term growth

- Real estate: House down payment or rental property investment

The Compound Effect of Frugal Living

A family that saves an extra $500 monthly through frugal living and invests it at 7% annual returns will have:

- $65,000 after 10 years

- $150,000 after 20 years

- $330,000 after 30 years

That’s the power of redirecting money from consumption to wealth building.

Your 30-Day Frugal Living Challenge

Ready to start your frugal living journey? Here’s a month-by-month action plan to build sustainable money-saving habits:

Week 1: The Foundation

- Track every expense for one week without trying to change anything

- Audit all subscriptions and cancel anything you haven’t used in 2 months

- Plan one week of meals based on grocery store sales

- Research better rates for one major expense (insurance, phone, internet)

Week 2: The Big Wins

- Get quotes for insurance to see if you can save money

- Calculate the true cost of your vehicle (payments, gas, insurance, maintenance)

- Identify one housing optimization opportunity (refinance, downsize, rent out space)

- Set up automatic transfers to savings for any money you’ve already saved

Week 3: Daily Life Optimization

- Try cooking at home for every meal for one week

- Research generic versions of 5 products you buy regularly

- Find three free or low-cost activities you actually enjoy

- Calculate cost-per-use for items you’re considering buying

Week 4: System Building

- Create a simple system for tracking savings in each category

- To avoid possible late fees, set up automatic bill pay.

- Plan next month’s major purchases around sales and seasonal timing

- Choose 3 frugal living strategies to focus on for the next quarter

The Truth About Frugal Living

Here’s what successful frugal families want you to know: it gets easier, and it gets better. The first few months require attention and effort as you build new habits and systems. But once those systems are in place, frugal living becomes automatic.

You’ll find yourself naturally gravitating toward better deals, making smarter purchasing decisions, and getting more satisfaction from the money you do spend because every dollar is intentional.

The families who master frugal living share a secret: they’re not sacrificing quality of life; they’re optimizing it. They’ve discovered that many expensive purchases don’t actually make them happier, while the financial security and freedom that come from living below their means absolutely do.

Frugal living isn’t about being cheap; it’s about being smart. It’s about having enough money for what matters most to you.

Your frugal living journey starts with a single decision to be more intentional with your money. Every family’s path looks different, but the destination is the same: financial freedom, reduced stress, and the ability to live according to your values rather than your budget constraints.

The question isn’t whether you can afford to live frugally, it’s whether you can afford not to.

Want a full year of money-saving ideas?

You can grab our 365 Frugal Living Tips printable, packed with practical strategies for every season and situation.

Real tips. Real savings. No fluff.