I left a well-paying job and transitioned to Army pay: Here’s What Happened

Most of them pause when I tell people we went from a well-paying job to Army pay. Then they ask the same question: “How did you do it?”

The truth is, we didn’t just survive that transition; we learned to live better on less.

We went from a comfortable California lifestyle, with two steady incomes and plenty of margin, to a new life in Georgia, living strictly on military pay. And when I say “strictly,” I mean it.

Our housing allowance was $1,450 per month, and our mortgage was $1,415. That left a grand total of $35.

Food? We were allotted $323. Most months, we spent about $325 to $350, close enough that I could tell you the total down to the last loaf of bread.

It was tight, but we were determined to make it work.

And right from the start, we decided on one rule: we would live within our allowances, no matter what.

That mindset became our foundation.

We saved everywhere we could, turning off lights, unplugging unused electronics, and cutting anything that didn’t matter. The basics made a difference. But soon, I noticed something odd that went beyond budgeting.

Our Electric Bill Was Double And No One Could Explain It

Something Was Off

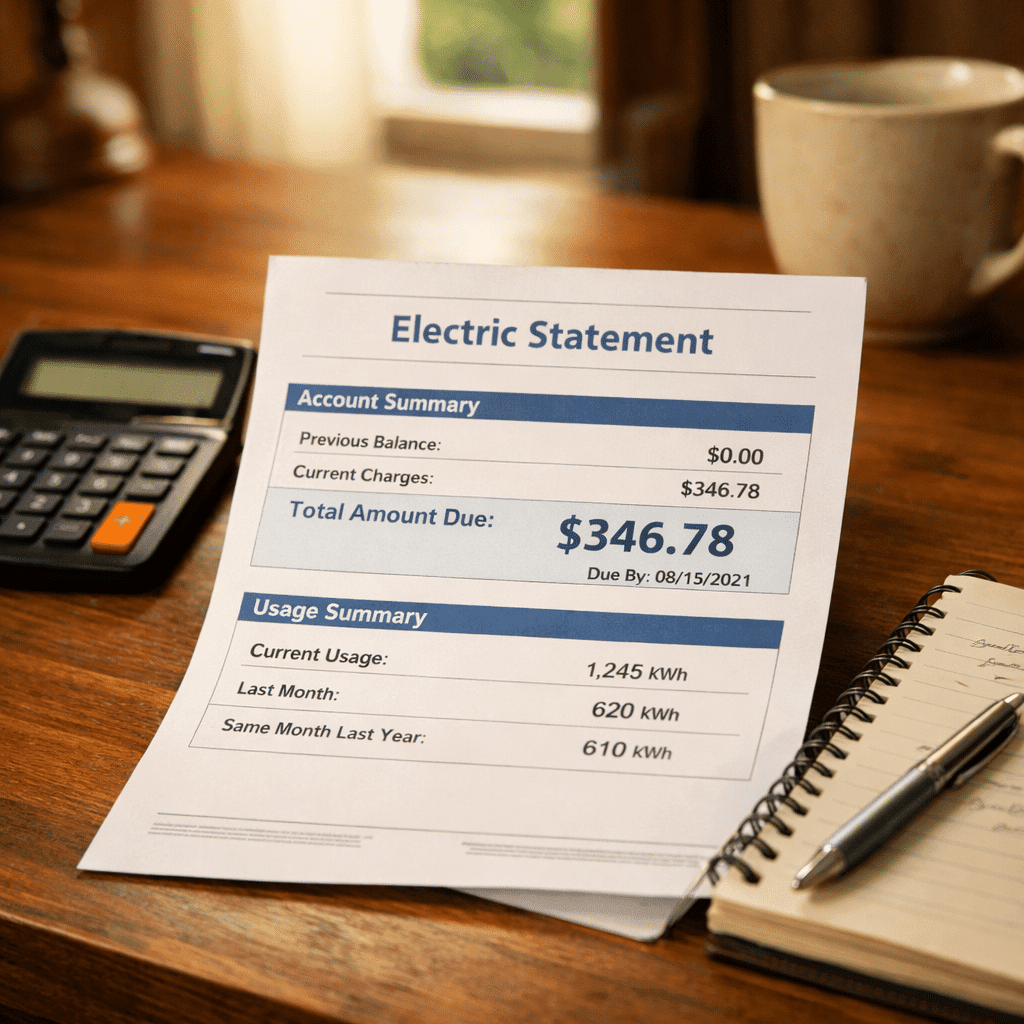

Our electricity bill was higher than I expected, a lot higher.

We had just purchased a newly built home, so I knew our usage should have been reasonable. My husband was gone most of the time, and our son was just two years old. It didn’t make sense (or cents) for the bill to be that high.

Asking Around Didn’t Help

So I started asking around the neighborhood.

Most of the neighbors avoided the question or brushed it off. They didn’t want to compare bills. That’s fine; money talk can make people uncomfortable. But still, I couldn’t shake the feeling that something wasn’t right.

So I called the electric company.

The first call ended with them telling me it was my usage. The second call ended the same way. By the third, they offered to send someone out, but only after I completed a long “energy checklist” to make sure I wasn’t the problem.

Still No Answers

I followed their list: checked lights, appliances, thermostat, water heater, you name it. Everything was normal.

Still, the bills kept coming, and they were double what I expected.

So I called again.

And again.

Finally, after weeks of persistence, someone admitted that there might be an issue in the area. A few days later, I got a call confirming it; they had been charging our entire neighborhood the builder’s rate instead of the homeowner’s rate.

They called it an “honest mistake.” I called it “expensive honesty.”

They credited my account, and I didn’t have to pay an electric bill for over three months. That moment taught me something valuable: awareness saves more than money; it saves your peace of mind.

Sometimes being frugal isn’t about cutting back; it’s about paying attention.

If you’re in a season where every dollar matters, listen to that little voice that says, “Something’s off.” Question it. Double-check it. Make that extra phone call.

Because sometimes the biggest savings come from the smallest hunches.

And if you’re wondering whether one income could even work for your family, I’ve linked my free

30 Minute One-Income Decision. It’s the same tool that helped us stay grounded during that transition, clear, simple, and honest about what’s possible.

Once we solved that issue, I started realizing how much opportunity was hiding in the details of everyday life. It wasn’t about coupons or extreme sacrifice; it was about noticing what others overlooked.

They Tried to Charge Me $989 for Water I Didn’t Use

The following year, there was another issue. We had a beautiful view behind our home. There was a gully between the houses, and one day I noticed workers back there doing some grading for a neighbor who was having runoff issues.

I didn’t think much of it at the time.

Then the next month, I got a water bill that didn’t make sense. It was extremely high, and they told me it would keep increasing based on usage.

I told them, that’s not possible. We’re not using that kind of water. And I mentioned that I had seen workers behind our home.

They dismissed it at first.

Then they told me I might have to split the cost with a neighbor, almost $1,000.

That’s when I knew something was wrong.

I said no. I’m not paying that. You need to come out and check this.

When they finally sent someone, I walked out there with them. They didn’t expect that.

And right away, they found the issue.

A pipe had been cut during the work behind our home.

At first, they still tried to say I’d be responsible for part of it.

I refused.

And eventually, they credited the full amount and resolved the bill.

That experience made something very clear to me.

There was money being lost in places most people don’t think to look.

How We Found Hidden Savings in Everyday Life

Back in 2005 to 2010, when we were living in Georgia, there were a lot more opportunities to save if you were paying attention.

Many restaurants offered buy-one, get-one-free deals. We found local buffets that gave military discounts, and we used punch cards, eat there a few times, and you’d earn a free meal or drinks.

There was one place we went to about once a week. My lunch was $5.95, and my oldest son ate free until age three. After that, it was only $2.99. By 2007, when my second son was born, he loved going there too.

So, for about $8 plus tip, we could all eat buffet-style, including desserts and ice cream (my husband was at work).

It wasn’t just about the cost. It gave me a break from cooking, and it became something we all looked forward to as a family.

Looking back, I wish those kinds of deals were still as common today.

But what that season taught me is this:

Those small wins added up fast.

It wasn’t about eating out all the time; it was about making smart choices when we did. We could enjoy meals together, even on a small budget, without feeling deprived.

How We Save Money Today

Today, it looks a little different, but the goal is the same.

We still look for those same kinds of opportunities, but now we use reward points from our credit cards to purchase gift cards for places like Amazon, Bath & Body Works, and restaurants like Cheddar’s.

It’s not the same as it was back then, but the principle hasn’t changed; small, intentional choices still add up.

Why Intentional Spending Works

Living better on less wasn’t about giving things up.

It was about being intentional, observant, and making what we had work.

Once we started paying attention to those hidden opportunities, the way we managed money changed completely. We didn’t feel limited; we felt in control. Every dollar had a purpose, and we made sure it worked for us.

At home, the grocery store became our second classroom.

It’s not that I didn’t know how to do these things before.

I just didn’t have to.

Before we moved to one income, we were living differently, and there wasn’t the same need to think this way.

But once things changed, these habits became part of our routine.

We weren’t starting over every day.

We were building on what we already had.

It made cooking feel simpler, not harder, and it took a lot of pressure off trying to come up with something new every night.

We started cooking double batches and freezing the extras. Grocery store loyalty programs helped too. Back then, if you paid attention, you could spot when stores rotated discounts every four to six weeks, so I would stock up when prices were at their lowest.

The Shift That Changed Everything

And here’s what surprised me the most.

After a few months of living like this, we were eating better than we ever had when our income was higher.

The difference wasn’t money.

It was intention.

That was one of the biggest mindset shifts for me. We didn’t lose comfort when we dropped to one income.

We gained control.

If you’re wondering whether your family could make this work, that’s exactly what the 30 Minute One-Income Decision is for. It helps you see, in black and white, what your true costs look like: housing, food, utilities, everything. Sometimes we assume it’s impossible until we see the math laid out clearly. You can try it using the link in the description below.

As I got more confident, I started treating saving like a game. Could I find one more place to shave $20 a month? Could I make the same meal for less by switching brands or stores? It became a challenge that actually felt exciting.

And as odd as it sounds, this new simplicity brought peace. We didn’t have to wonder where the money was going; we knew.

There’s a freedom that comes when you stop chasing “more” and start managing “enough.”

The 5 Lessons That Made One Income Work

1. Awareness Beats Anxiety.

The moment you start tracking your money, the fear begins to settle. You’re no longer guessing, you’re looking at real numbers. Even if those numbers aren’t what you hoped, they give you something to work with.

For us, awareness wasn’t about perfection. It was about knowing what was coming in, what was going out, and where things didn’t make sense, like those bills that didn’t add up.

When you can see your money clearly, you can make decisions calmly instead of reacting out of fear.

2. Creativity Is More Valuable Than Coupons.

We didn’t need hundreds of discounts; we needed better ideas.

Creativity showed up in simple ways: stretching meals, using what we already had, finding patterns in pricing, and making small adjustments that worked for our life.

When you shift from “what can I cut?” to “how can I make this work?” you stop feeling restricted and start feeling capable.

That’s when things begin to change.

3. Keep Joy in the Budget.

Even on a tight allowance, we made space for small moments that mattered, a family meal out, a simple outing, something for the kids.

Because a budget without joy doesn’t last.

If everything feels like a sacrifice, you’ll eventually push back against it. But when your budget reflects your real life, what you value, what you enjoy, it becomes something you can actually stick with.

A good budget shouldn’t just control your money. It should support your life.

4. Adjust, Don’t Abandon.

Some months didn’t go as planned. Car repairs, school needs, unexpected travel—life still happened.

But instead of saying “this isn’t working,” we learned to ask, “what needs to shift?”

Maybe we pulled back in one area to cover another. Maybe we delayed something instead of eliminating it.

That mindset kept us moving forward.

Because most plans don’t fail, they just need adjusting.

5. Peace Is the Real Profit.

At some point, everything shifted.

We stopped measuring success by income and started measuring it by how we felt, peace, time, and freedom.

We weren’t chasing more anymore. We were managing what we had with intention.

And that brought a kind of stability we didn’t have before, even when we were earning more.

That shift didn’t happen overnight. It came from small decisions, repeated over time, and a willingness to see things differently.

Looking back now, I realize our decision to live on one income wasn’t a sacrifice; it was a strategy.

It forced us to pay attention, to make intentional choices, and to build a system that actually supported our life.

We went from six figures to Army pay, but we didn’t lose anything that truly mattered. If anything, we gained clarity, control, and peace.

If you’ve ever thought about making the same shift, start by knowing your numbers. That’s what gave us the confidence to move forward. You can use the free 30-Minute One-Income Decision. It’s private, it’s simple, and it’s the same tool that helped us map out this journey.

Living better on less doesn’t happen by chance. It happens by choice; one small, intentional decision at a time.

So whether you’re trying to save, simplify, or just breathe again, start where you are.

It can feel like you need six figures to live well, and in some places, you might.

But no matter your income, having a plan that makes sense will always matter more.

You just need a plan that works for your life. Or, in my case, makes cents.