Master Your Money: Essential Budgeting for 2026

Whether you are working your way out of debt, living paycheck to paycheck, or looking to build more margin into your finances, this guide provides 25 actionable budgeting strategies that work in today’s economic reality.

The Budgeting Reality Check That Will Change Everything

Here’s the truth no one talks about: 70%+ of Americans are saving less money in 2026 than they were three years ago. Not because they’re irresponsible, but because traditional budgeting advice is completely out of touch with today’s economic reality.

While financial “experts” keep pushing the same old 50/30/20 rule, real families are drowning trying to make outdated formulas work in a world where rent takes 40% of income and groceries cost 25% more than last year.

In this comprehensive guide, you will learn:

- ✓ The 25 proven budgeting strategies that actually work in 2026’s economic climate

- ✓ How to adapt budgeting methods to your specific location and cost of living

- ✓ The psychology behind why traditional budgets fail and how to overcome it

- ✓ Advanced automation systems that build wealth without constant monitoring

- ✓ Real-world strategies from families who’ve successfully escaped paycheck-to-paycheck living

Why Most Budgets Fail (And How to Fix It by Location)

When our family transitioned to one income, I learned very quickly that generic budgeting advice didn’t always fit our situation. We weren’t trying to cut luxury vacations or expensive hobbies. We were trying to make everyday expenses fit within a single paycheck while raising a family. That’s why I believe budgeting has to reflect your real life, not someone else’s formula.

The biggest mistake people make is treating budgeting like a diet, restrictive, temporary, and doomed to fail. Instead, think of budgeting as a location-aware money management system that permits you to spend on what matters while automatically building wealth.

Let’s be honest: traditional budgeting advice hasn’t kept up with 2025 realities. With inflation eating into every paycheck and housing costs varying dramatically by state, the old “just spend less” advice feels insulting. You need strategies that actually work in your specific location and economic reality.

$6,000 Average annual savings with zero-based budgeting

70%+ of Americans are saving less due to inflation (2026)

15-20% More savings with structured budgeting methods

3.5-5% Current high-yield savings rates (2026)

The 2026 Regional Budgeting Reality Check

- Geographic Impact: Housing costs range from $145K median (Mississippi) to $730K (Hawaii) – your location determines your budget strategy

- Income Variations: Median household income spans from $46K (Mississippi) to $155K+ (San Jose) – traditional percentages don’t work everywhere

- Cost Adjustments: The 50/30/20 rule is a starting point, not a fixed formula. High-cost areas may require a 60/30/10 or 65/25/10 budget, while more affordable regions may allow a 45/30/25 approach with a higher savings rate.

- Local Opportunities: Regional credit unions offer 4-6% savings rates vs. 0.38% national bank average

Your State’s Budget Reality (2026 Data)

High-Cost States

CA, NY, MA, HI, AK: Median home prices $425K and above; groceries 20 to 50 percent above the national average. Budget strategy: 60/25/15 split, prioritize house hacking or roommates, maximize employer benefits aggressively.

Affordable States

MS, AR, WV, KS, OK: Median homes under $190K, groceries 10 to 20 percent below average. Strategy: A 45/30/25 split allows aggressive savings and accelerated wealth building.

Growth Markets

TX, FL, CO, NC, GA: Rising costs but strong job markets. Strategy: Lock in housing costs early, negotiate salary based on inflation, build emergency fund first.

Arizona Advantage

Phoenix and Tucson: Moderate costs ($73K median income, $420K median home), strong local credit union options. No state income tax advantage remains. Groceries run roughly 3 percent above the national average. Strategic shopping with loyalty programs reduces that gap significantly

The Top 3 Budgeting Methods That Actually Work

Zero-Based Budgeting

Best for: Serious savers & debt elimination

How It Works:

Give every dollar a job before you spend it. Income minus expenses equals zero.

The Formula:

- Calculate monthly take-home pay

- List all expenses (needs, wants, savings)

- Assign every dollar to a category

- Track and adjust monthly

Success Rate: Users save an average of $6,000 in the first year

One of the biggest lessons I learned over the years was that money works better when it has a purpose before it arrives. We didn’t always use formal budgeting software, but we did assign jobs to our income. Knowing where the money needed to go before the month began reduced a lot of stress and uncertainty.

50/30/20 Rule (2026 Geographic Adjustments)

Best for: Budgeting beginners & simple tracking

Traditional Split:

- 50% Needs: Housing, utilities, groceries, insurance

- 30% Wants: Entertainment, dining out, hobbies

- 20% Savings: Emergency fund, retirement, debt payoff

2026 Regional Adjustments:

High-Cost States (CA, NY, MA): 60/25/15 or 65/20/15

Moderate States (TX, FL, CO): 55/30/15

Low-Cost States (MS, AR, OK): 45/30/25

Income Thresholds by Region:

San Jose area: Need $115K+ for traditional split

NYC area: Need $90K+ for traditional split

National average: Works at a $68K+ household income

Success Rate: Works for 70% of households when adjusted for location

Best Tool: Regional budget calculators + Monarch Money

Digital Envelope Method

Best for: Impulse spenders & visual learners

Modern Implementation:

Use apps to create virtual “envelopes” for spending categories. When an envelope is empty, no more spending until next month.

Key Categories:

- Groceries

- Gas/Transportation

- Entertainment

- Dining Out

- Shopping/Miscellaneous

Success Rate: Reduces overspending by 25-40%

Best Tool: Goodbudget (free) or PocketGuard

25 Actionable Budgeting Tips for 2026

1. Automate Everything

Action: Set up automatic transfers to savings on payday. Impact: Removes willpower from the equation and ensures consistent progress toward goals.

2. Use Local High-Yield Savings

Local credit unions are offering 3.5 to 5 percent APY in 2026 versus the national bank average of around 0.45 percent. Examples: Bellco CU (CO), OneAZ CU (AZ), Vibrant CU (national access). Verify current rates before opening. A $10,000 balance earns $350 to $500 annually at credit union rates versus $45 at the average national bank.

3. Track in Real-Time

Use budgeting apps with bank sync to categorize expenses as they happen. Catching overspending in week two of the month is far more useful than discovering it in the last few days.

4. Build a Mini Emergency Fund First

Goal: $1,000-2,000 before tackling debt aggressively. Reason: Prevents new debt when small emergencies arise.

5. Audit Subscriptions Every Quarter

Average savings: $200 to $400 per year. Cancel unused services, negotiate better rates, and choose annual plans over monthly billing. With the number of subscription services now available, quarterly audits are more effective than annual ones.

Average savings: $200-400 per year. Action: Cancel unused services, negotiate better rates, choose annual plans over monthly.

6. Regional Meal Planning Strategy

High-cost states: Save $300 to $500 per month on groceries with planned shopping. Arizona: Save $200 to $350 per month with store loyalty cards and seasonal produce. Low-cost states: Save $150 to $250 per month. Meal planning works because it eliminates unplanned purchases, reduces food waste, and removes the last-minute decisions that lead to expensive takeout.

Meal planning has probably saved our family thousands of dollars over the years. Not because we ate perfectly, but because we knew what we already had, planned around sales, and avoided those extra grocery trips that somehow add up to another $50 or $100.

7. Create Sinking Funds

Concept: Save monthly for predictable irregular expenses: car repairs, holiday gifts, insurance renewals, medical copays. Irregular expenses are not surprises. They are planned costs without a plan. A sinking fund fixes that.

8. Geographic Housing Strategy

High-cost areas: House hacking, roommate arrangements, or considering within-metro relocation can save $1,500 to $2,500 per month. Affordable areas: Buying versus renting often makes stronger financial sense. Growth markets: Locking in housing costs now before further appreciation reduces long-term risk.

9. Slash Utility Bills

Quick wins: Smart thermostats, LED lighting, and unplugging devices on standby produce $200 to $500 in annual savings for the average household. Arizona households that use level billing plans avoid summer utility shock and can budget a consistent monthly amount year-round.

10. Optimize Transportation

Strategies: Walk or bike when realistic, consolidate errands into one trip, and maintain your vehicle on schedule. Deferred maintenance consistently costs more than the maintenance itself. Savings range from $50 to $200 per month depending on driving habits.

11. Use the 24-Hour Rule

Practice: Wait 24 hours before non-essential purchases over $50. Result: Eliminates 60-70% of impulse buying

12. Switch to Store Brands

Savings: 20-40% on groceries and household items. Strategy: Start with basics like rice, pasta, cleaning supplies, then expand.

13. Leverage Cashback Apps

Stack rewards: Use cashback credit cards + apps like Rakuten. Annual earning potential: $300-800 on existing purchases.

14. Geographic Bill Negotiation

High-cost areas: Emphasize competitor rates (more options). Rural areas: Mention loyalty/limited alternatives. Script: “I’ve lived here X years, what’s your retention rate?” Best results: Urban 70%, rural 45%

15. Use Zero-Sum Spending

Rule: For every new recurring expense, cancel an existing one of equal value. Benefit: Prevents subscription creep and lifestyle inflation.

16. Maximize Employer Match

Priority: Contribute enough to get full 401(k) match before other investments. Return: Instant 50-100% return on investment.

17. Automate Debt Payments

Strategy: Set autopay for minimums on all accounts plus a fixed extra amount toward the highest-rate balance. Automation removes missed payments from the equation and keeps the payoff timeline moving without requiring monthly discipline.

18. Try a No-Spend Challenge

Duration: Start with one week monthly. Rules: Only essentials (groceries, gas, bills). Result: Reset spending habits and boost savings.

19. Round Up Savings

Method: Use apps that round purchases to nearest dollar and save the change. Average: $30-60 monthly in automatic micro-savings.

20. Review Spending Weekly

Timing: Every Sunday, spend 15 minutes reviewing the past week. Focus: Identify surprises and plan adjustments for the coming week.

21. Budget for Fun

Allocation: Set aside money for entertainment guilt-free. Psychology: Planned fun spending prevents budget rebellion and binge spending.

22. Use Percentage-Based Goals

Example: Save 1% more each quarter rather than fixed amounts. Advantage: Goals scale with income increases naturally.

23. Practice Budget Flexibility

Approach: If you overspend in one category, underspend in another. Benefit: Maintains overall budget without guilt or giving up.

24. Use Budget-Friendly Alternatives

Examples: Library instead of bookstore, workout videos vs. gym, potlucks vs. restaurants. Mindset: Find ways to enjoy life for less.

25. Celebrate Small Wins

Recognition: Acknowledge every $500 saved, debt milestone, or month under budget. Psychology: Positive reinforcement builds long-term habits.

Best Budgeting Apps & Local Banking for 2025

Top Paid Options

YNAB (You Need A Budget)

Approximately $109 to $149/year — verify current pricing at ynab.com

Best for: Zero-based budgeting & debt payoff

Pros: Proven methodology, strong community, claims $6,000 first-year savings

Cons: Steep learning curve, expensive

Free trial: 34 days (1 year free for students)

Monarch Money

$99.99/year

Best for: Complete financial tracking & couples

Pros: Investment tracking, net worth monitoring, household sharing

Cons: Most expensive, complex setup

Free trial: 7 days

Quicken Simplifi

Approximately $47 to $71/year

Best for: Simple, Mint-like experience

Pros: Clean interface, spending plans vs budgets

Cons: Limited advanced features

PocketGuard Plus

$74.99/year

Best for: Simplicity & “spendable money” tracking

Pros: Shows money left after bills, debt payoff plans

Cons: Limited features beyond basics

Best Free Options

Goodbudget

Free tier available (Premium approximately $80/year)

Best for: Envelope budgeting beginners

Free includes: 20 envelopes, 2 devices

Limitation: Manual entry only on free tier

NerdWallet

Completely Free

Best for: Basic tracking with credit monitoring

Pros: No paid version, credit score included

Cons: Ads, limited budgeting features

Rocket Money

Free tier + premium $6-12/month

Best for: Subscription management

Pros: Cancel unwanted subscriptions, bill negotiation

Unique: Choose-your-price premium model

Regional Banking Opportunities

West Coast & Southwest

| California | Golden 1 Credit Union | 3.5%+ (verify current) |

| Arizona | OneAZ Credit Union | Competitive — check current rates |

| Arizona | Desert Financial CU | Above national bank average |

| Colorado | Bellco Credit Union | Competitive — check current rates |

| National Access | Alliant Credit Union | Competitive — check current rates |

| National Access | Vibrant Credit Union | $5 membership, check current rates |

Mountain States

Bellco Credit Union (CO): 4.50% APY

Peak Bank (ID): 4.35% APY online

Access: Most allow membership via small donations

Midwest

MSU Federal Credit Union (MI): 4.00%+ APY

Advantage: Lower cost of living + higher savings rates

Strategy: Maximize savings rate advantage

National Access

Alliant Credit Union: 3.10% APY, $0 to join

Vibrant Credit Union: 4.50% APY, $5 membership

DCU: 6.17% on first $1,000, then 0.16%

Regional Emergency Fund Strategy for 2026

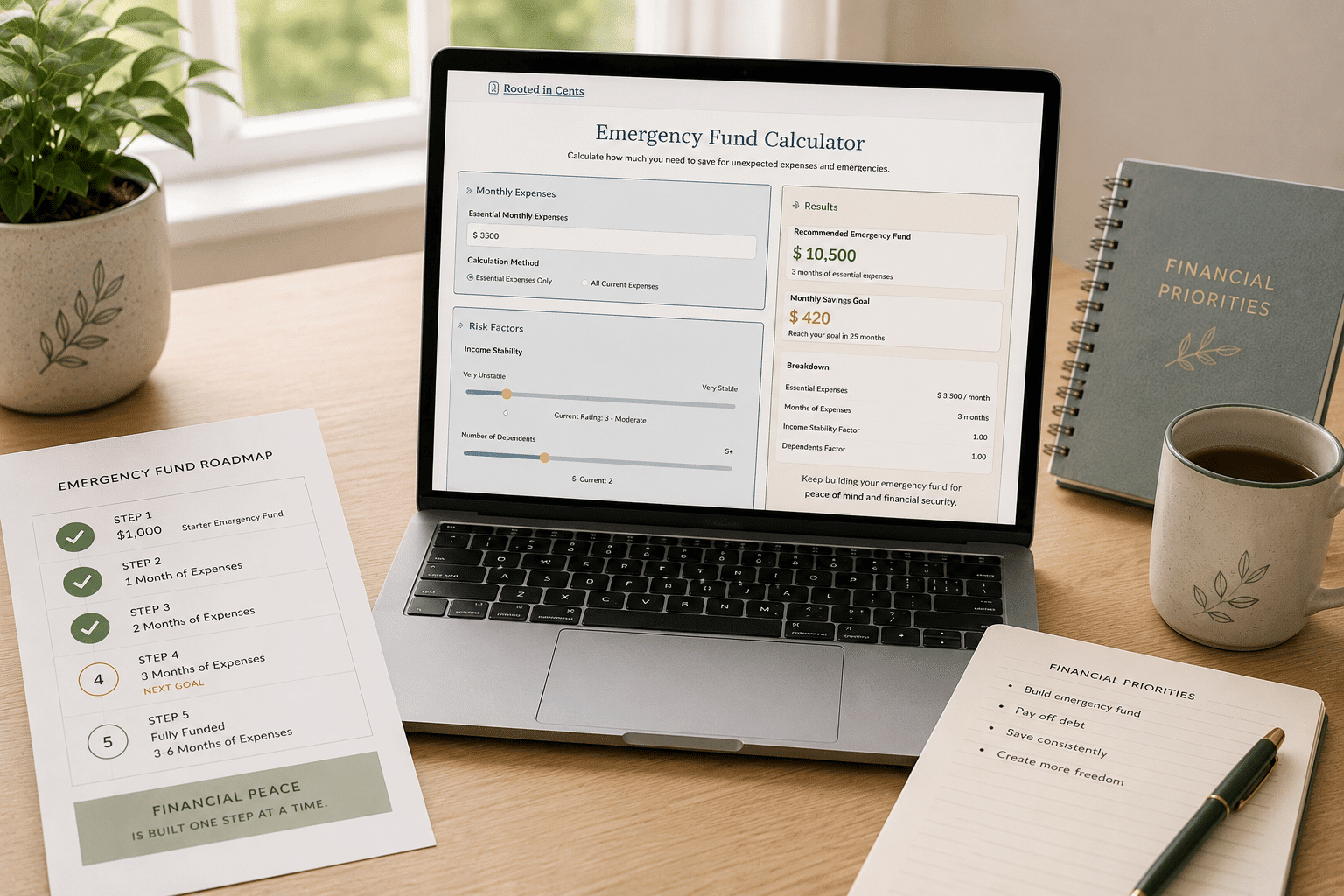

During my years in aerospace and telecommunications, I saw firsthand how quickly income can change. Overtime disappeared. Production slowed. Layoffs happened. Having cash set aside didn’t solve every problem, but it gave our family time to make decisions without panicking. An emergency fund isn’t just about money. It’s about buying yourself options when life changes unexpectedly.

Plan smarter with my Emergency Fund Calculator, which quickly estimates the ideal savings you need based on your location and unique circumstances.

Calculate by Location

High-cost areas (CA/NY/MA): 9-12 months of expenses

Moderate cost areas (TX/FL/CO): 6-9 months

Low-cost areas (MS/AR/OK): 4-6 months

Single-industry towns or volatile sectors: Add 3 months to any baseline

Regional Starter Fund Goals

High-cost areas: $2,500-5,000 starter fund (1 to 2 months of minimum local rent)

Moderate areas: $1,500-2,500

Low-cost areas: $1,000-1,500

Income-Adjusted Full Fund Goals

| Location | Approximate Income | Full Fund Target Range |

|---|---|---|

| San Jose area | $155K | $77K to $116K |

| National median | $80K | $40K to $60K |

| Mississippi | $46K | $15K to $28K |

General guideline: Auto-save 10 to 15 percent of the regional median income into the emergency fund until fully funded.

Your 90-Day Budgeting Action Plan

Transform your finances in three months with this step-by-step checklist:

Month 1: Foundation

- Track every expense for 30 days.

- Choose budgeting method (50/30/20, zero-based, or envelope)

- Open a high-yield savings account

- Set up automatic savings transfer

- Cancel 3+ unnecessary subscriptions

Month 2: Optimization

- Build $1,000 mini emergency fund

- Implement weekly meal planning

- Negotiate 2+ recurring bills

- Choose a debt payoff strategy (snowball vs avalanche)

- Start 2-3 sinking funds (car, holidays, etc.)

Month 3: Acceleration

- Increase savings rate by 1-2%

- Optimize cashback rewards system

- Start one side income stream

- Research investment basics (after emergency fund)

- The Complete 90-day financial review

Advanced Strategies for 2026

The Sinking Fund System

Sinking funds transform large irregular expenses into manageable monthly savings. Instead of being caught off guard by a $1,200 car repair, you save $100 each month in a dedicated car maintenance fund. When the expense arrives, the money is already there.

Essential Sinking Fund Categories:

- Car expenses: Repairs, maintenance, insurance ($100-150/month)

- Home maintenance: 1% of home value annually ($200/month for $240K home)

- Holiday/gifts: Christmas, birthdays, weddings ($75-100/month)

- Technology: Phone/laptop replacements ($50/month)

- Medical expenses: Copays, prescriptions, dental ($50-75/month)

Regional Inflation-Beating Techniques

While year-over-year inflation has moderated from its 2022 peaks, the cumulative price increases since 2020 are permanent in most categories. Regional strategies that maximize your purchasing power remain essential in 2026.

Regional Inflation-Beating Techniques

While year-over-year inflation has moderated from its 2022 peaks, the cumulative price increases since 2020 are permanent in most categories. Regional strategies that maximize your purchasing power remain essential in 2026.

High-Inflation Areas (West Coast, Northeast)

- Local credit unions: 3.5 to 5 percent APY versus 0.45 percent at national banks

- COLA advantages: Negotiate salary increases based on local inflation data

- Cross-border shopping: Major purchases in neighboring lower-cost states

Moderate-Cost Growth Areas (TX, FL, CO, AZ)

- Property tax appeals in rising markets — worth checking annually

- No or low state income tax: TX, FL, and AZ all provide this advantage

- Growing economies create side income and freelance opportunities

Low-Cost Areas (Midwest, South)

- Lower costs enable higher savings rates, which compound significantly over time

- Remote work at coastal salaries with local cost of living is a genuine wealth-building opportunity

- Focus on investment and wealth acceleration once emergency fund is complete

The Automation Advantage

Setting up finances to run on autopilot removes the monthly decision fatigue that causes most budgets to fail after three to four months.

- Direct deposit splits: Paycheck automatically divided between checking, savings, and investment accounts on arrival

- Bill autopay: All fixed expenses paid automatically — no late fees, no missed payments

- Investment automation: 401(k), IRA, and taxable investments funded automatically each month

- Sinking fund transfers: Each fund receives its monthly allocation automatically before discretionary spending begins

State-by-State Budget Reality Check(2026)

Here’s how the same household income performs across different states in 2026:

$75,000 Household in California

| State | Housing (est.) | Groceries (family of 4) | Savings Potential | Key Strategy |

|---|---|---|---|---|

| California | $3,800/mo (61%) | $1,200/mo | $200 to $500/mo | House hack, maximize employer benefits |

| Texas | $2,300/mo (37%) | $1,000/mo | $1,000 to $1,500/mo | No state income tax, aggressive wealth building |

| Mississippi | $1,500/mo (24%) | $860/mo | $2,000+/mo | Wealth acceleration, property investment |

| Colorado | $2,850/mo (46%) | $1,050/mo | $600 to $900/mo | Local credit unions, outdoor lifestyle on budget |

| Arizona | $2,700/mo Phoenix, $2,200 Tucson | $1,100/mo | $800 to $1,200/mo | No state income tax, strong local credit unions |

Regional Grocery Cost Impact (2026)

Weekly grocery spending for family of four across regions:

| State | Estimated Weekly Cost (family of 4) | Monthly Total |

|---|---|---|

| Hawaii | $340 | $1,360 |

| California | $300 | $1,200 |

| Arizona | $278 | $1,110 |

| National Average | $270 | $1,080 |

| Texas | $252 | $1,008 |

| Wisconsin | $222 | $888 |

What this means: Grocery costs vary significantly by region. While Arizona families often spend less than those in higher-cost states like Hawaii, food costs can still put pressure on a household budget. Meal planning, loyalty programs, seasonal produce, and reducing food waste can help lower grocery spending regardless of where you live.

Your Location-Specific Next Steps

Budgeting is not about restriction. It is about optimizing for your geographic reality while building stability over time. Your location shapes your strategy, but it does not determine your outcome.

High-Cost Area Residents

Start with housing optimization and local credit union research. Finding $500 in monthly savings has a compounding impact in a high-cost environment.

Low-Cost Area Residents

Focus on savings rate acceleration. Your dollar goes further. Leverage that by building your emergency fund faster and moving to wealth-building sooner.

Arizona Residents

You have strong local credit union options and a no state income tax advantage. Combine those two features with a structured budget and the savings accumulate faster than most people expect. Verify current rates at OneAZ CU, Desert Financial CU, and Arizona Financial CU before opening new accounts.

Everyone

Open a local credit union account this week. The interest rate difference between a credit union and the average national bank on a $10,000 emergency fund is real money. Start there.

Our family has lived on one income for more than twenty years. We’ve navigated job changes, unexpected expenses, relocations, and economic uncertainty. What I’ve learned is that budgeting isn’t about perfection. It’s about creating enough stability and flexibility that life doesn’t completely derail your finances when something unexpected happens.

Final Thoughts

Budgeting successfully in 2026 requires more than good intentions; it demands smart strategies tailored to your geographic reality. The 25+ techniques in this guide aren’t just money tips; they’re location-aware wealth-building tools designed for real households facing real costs in real communities.

Whether you’re leveraging Arizona’s credit union advantages, maximizing savings in the affordable Midwest, or optimizing high incomes in expensive coastal markets, remember that small, consistent actions compound into life-changing results.

Your financial freedom isn’t determined by where you live, but by how well you understand and leverage the opportunities your location provides.

Pingback: Why Your Monthly Budget Fails With Bi-Weekly Pay - Digital Financial Tools

Pingback: What Are Debt Relief Credit Cards? A Beginner’s Guide - Spend Less and Live More

Pingback: 10 Proven Budgeting Strategies to Take Control of Your Finances - Spend Less and Live More

Pingback: Young Adults Living With Parents: What Families Are Navigating Right Now - Helping You Navigate Financial Transitions