Complete Roadmap to Thrive on One Income

Here’s the one-income truth: Nearly 30% of households rely primarily on a single income, showing that one-income living remains a reality for millions of families.

In this comprehensive one-income guide, you will learn:

- ✓ 6-month strategic transition plan for successful income reduction

- ✓ Hidden cost analysis showing true value of second incomes

- ✓ Budget optimization techniques specific to single-income families

- ✓ Emergency fund building and financial security strategies

- ✓ Flexible income generation options for stay-at-home partners

You’re staring at the calculator for the third time this week, running the numbers again. Can your family really make it on just one income? Whether you’re considering staying home with a new baby, caring for aging parents, or one of you is facing job uncertainty, the thought of losing an entire paycheck feels overwhelming.

Here’s what nobody tells you: one-income living isn’t just possible; it can actually improve your family’s quality of life and financial stability when done strategically. Nearly 30% of families successfully live on one income, and many report less stress, stronger family bonds, and, surprisingly, better long-term financial outcomes.

But here’s the catch: it requires intentional planning, not wishful thinking.

Why Your Current Budget Math Might Be Wrong

Before you panic about cutting your household income in half, let’s talk about what you’re really losing and gaining.

The Hidden Costs of Two-Income Living

That second paycheck comes with expenses you might not be calculating:

- Childcare costs: The average family spends $12,000-$20,000 annually per child

- Commuting expenses: Gas, car maintenance, parking can easily hit $3,000-$5,000 yearly

- Work wardrobe: Professional clothing, dry cleaning, appearance maintenance

- Convenience costs: Takeout meals, housecleaning, time-saving purchases

- Higher tax bracket: Two incomes often push families into higher tax rates

When you subtract these work-related expenses, you might discover that the second income is netting far less than you thought. Some families find they’re only truly gaining $800-$1,200 monthly after all costs, a much more manageable gap to bridge.

The Real Benefits You’ll Gain

One-income living offers advantages that don’t show up on spreadsheets:

- Time to meal plan and cook, dramatically reducing food costs

- Ability to shop sales, use coupons, and make strategic purchases

- Reduced wear on vehicles and household stress

- Flexibility to handle family emergencies without missing work

- Opportunity to develop money-saving skills and side income

- The Strategic Transition: Your 6-Month Preparation Plan

Successful one-income families don’t just quit their jobs and hope for the best. They prepare strategically.

Months 1-2: Financial Foundation Assessment

Calculate your true numbers. Track every expense for two months, then categorize them into

- Essential expenses (housing, utilities, food, transportation, insurance)

- Work-related expenses that would disappear

- Lifestyle expenses you could adjust

- Debt payments and savings goals

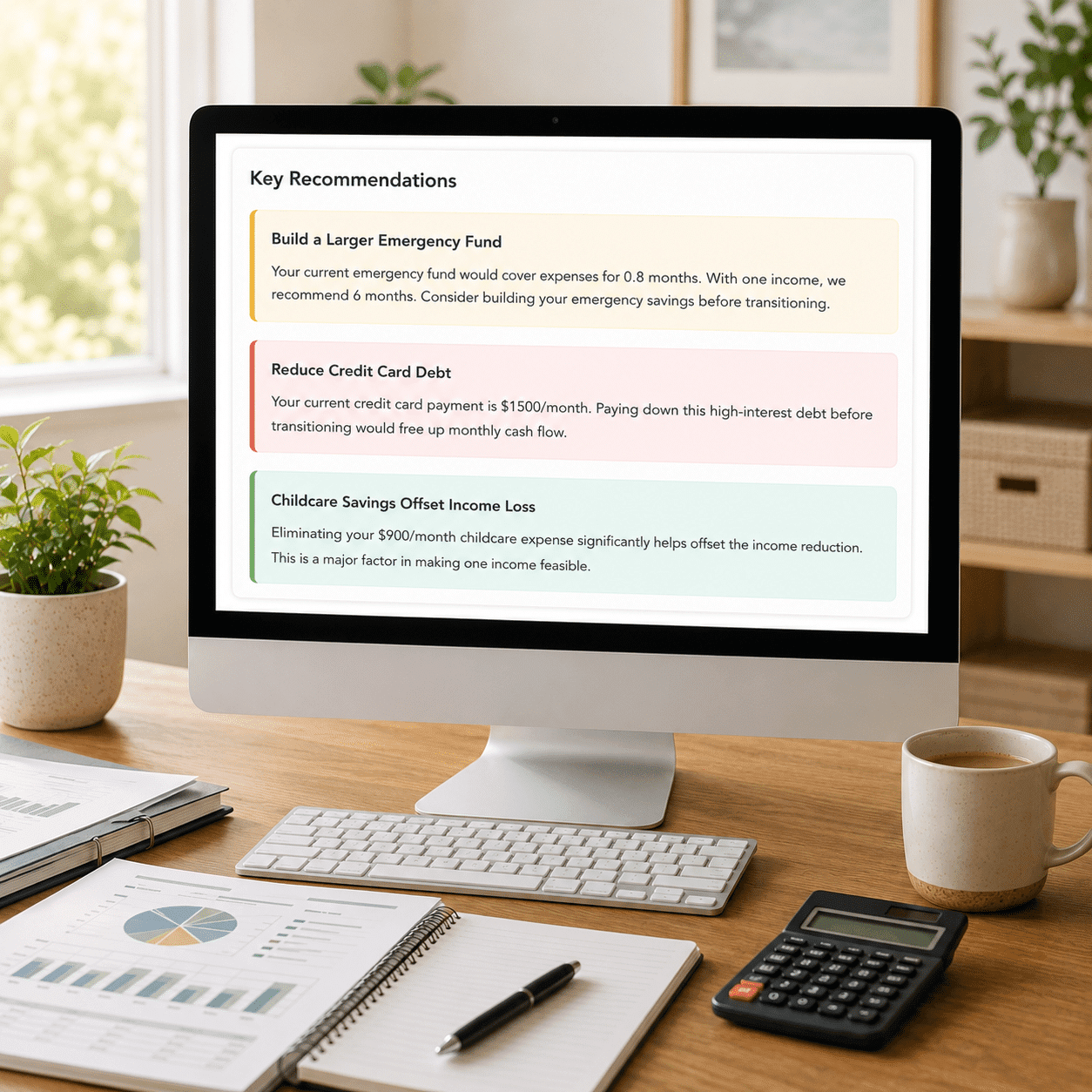

Build your emergency fund. Single-income families need larger safety nets. Aim for 6-12 months of essential expenses before making the transition. The process might seem daunting, but remember you still have two incomes during this preparation phase.

Months 3-4: Debt Elimination and Budget Optimization

Attack high-interest debt aggressively. Credit card payments will feel much heavier on one income. Use your current two-income situation to eliminate as much debt as possible.

Practice living on one income. Put the second paycheck directly into savings for two months. This method serves two purposes: it builds your emergency fund faster and lets you test-drive the lifestyle changes before they become permanent.

If you struggle during this practice period, you’ll know exactly where to adjust before making the real transition.

Months 5-6: Systems and Safety Nets

Research healthcare options. If the working spouse’s job provides health insurance, you’re set. If not, research marketplace options, consider a job with benefits, or look into healthcare sharing plans.

Set up income replacement strategies. Even if the non-working spouse isn’t planning to earn money initially, having systems in place for quick income generation provides peace of mind. Such solutions might include freelance skills, part-time remote work opportunities, or a small business framework.

Making Every Dollar Count: The One-Income Budget That Actually Works

Budgeting on one income isn’t just about cutting expenses; it’s about maximizing the value of every dollar you spend.

The 70-20-10 Rule for Single-Income Families

Forget traditional budgeting percentages designed for two-income households. Here’s what works for single-income families:

- 70% for essential living expenses: Housing, utilities, food, transportation, insurance, minimum debt payments

- 20% for goals and emergencies: Emergency fund maintenance, debt payoff, retirement savings

- 10% for lifestyle and flexibility: Entertainment, dining out, personal spending

This framework ensures you’re covering necessities while still making progress toward financial goals and maintaining some quality of life.

The Strategic Shopping Revolution

Having one parent home creates opportunities for significant savings that working parents can’t access:

Master the sales cycle. Grocery stores follow predictable patterns: meat goes on sale every 6-8 weeks, and pantry staples every 12 weeks. Stock up during sales and avoid paying full price.

Become a coupon strategist (not an extreme couponer). Concentrate on items that are genuinely useful for your family. For best effect, combine shop sales with manufacturer coupons. Even saving $30-50 weekly adds up to $1,500-2,600 annually.

Embrace bulk cooking and preservation. Cook large batches when ingredients are cheap, then freeze portions. This process turns expensive convenience foods into budget-friendly homemade options.

Income Diversification: Multiple Streams on One Salary

Smart one-income families don’t rely solely on a single paycheck. They create multiple, smaller income streams that add security without the overhead of traditional employment.

The Stay-at-Home Spouse Income Toolkit

Freelance your existing skills. Writing, graphic design, bookkeeping, tutoring, and virtual assistance are many professional skills that translate perfectly to part-time, remote work that fits around family schedules.

Monetize your home. Rent a room to a boarder, offer childcare for one or two other children, host foreign exchange students, or create a home-based business like meal prep services or online tutoring.

You can also engage in seasonal and project-based work. Tax preparation, holiday retail, substitute teaching, or seasonal landscaping provide income boosts during specific times without year-round commitment.

Maximizing the Primary Income

The working spouse’s income becomes even more critical, so optimize it strategically:

- Negotiate aggressively: With more financial pressure on this single income, don’t be modest about asking for raises, better benefits, or flexible arrangements

- Maximize tax advantages: Contribute to retirement accounts, use FSAs for medical expenses, and take advantage of all available deductions

- Develop recession-proof skills: Invest in professional development that makes the working spouse indispensable and marketable

The Psychology of One-Income Success

The biggest challenges of one-income living aren’t financial; they’re emotional and social. Here’s how to navigate them successfully.

Financial Contribution Redefined

The spouse who does not work frequently feels as though they are not making a financial contribution. This kind of thinking can hinder your progress. Rather, acknowledge their important contributions:

- Using meal planning and clever buying to save money

- Eliminating daycare costs valued between $15,000 and $25,000 per year

- Overseeing the administration and upkeep of the home and administration

- Creating family stability that allows the working spouse to focus on career advancement

Managing Social Pressure and Judgment

You’ll encounter people who question your choice, especially in communities where dual incomes are the norm. Prepare responses that shut down judgment while reinforcing your confidence:

“We’ve looked at the numbers, and this option is better for our family’s goals.”

“The extra money is nice, but the flexibility it gives us is worth more.”

“We’re not just looking for short-term income; we’re also looking for long-term financial stability.”

Keeping Your Own Goals and Identity

The spouse who doesn’t work shouldn’t ignore their family duties. Keep your interests, personal ambitions, and job aspirations for the future. This could mean:

- Programs for certification or continued education

- Volunteering that promotes skill development and networking

- Hobbies or artistic endeavors that bring personal satisfaction

- Creative projects or hobbies that provide personal fulfillment

- Clear re-entry plans for future employment if desired

Crisis-Proofing Your One-Income Life

Single-income families face higher financial risk if something happens to the working spouse. Here’s how to protect your family:

Insurance as Your Safety Net

Life insurance is non-negotiable. The working spouse should carry enough life insurance to replace their income for 10–15 years, giving the surviving spouse time to develop career skills and find employment.

Disability insurance protects your most valuable asset. Your ability to earn income is more valuable than your house or car. Short-term and long-term disability insurance ensure income continues if the working spouse becomes unable to work.

Building Recession-Resistant Skills

Both spouses should maintain marketable skills, even if only one is currently working:

- Keep professional licenses and certifications current

- Stay connected to industry networks and trends

- Develop skills that are always in demand (healthcare, education, skilled trades)

- Create multiple potential income streams rather than relying on traditional employment

Long-Term Wealth Building on One Income

One-income families can still build substantial wealth, it just requires different strategies than dual-income households.

The Tortoise Approach to Investing

You might not be able to max out retirement accounts immediately, but consistent, smaller contributions compound powerfully over time.

- Start with employer 401(k) match if available—this is free money

- Open a Roth IRA and contribute even $50-100 monthly

- Use tax refunds and bonuses for retirement contributions

- Some families choose permanent life insurance products as part of a broader financial plan, but it’s important to compare costs, benefits, and alternatives before making a decision.

Real Estate as Wealth Building

Homeownership becomes even more valuable for one-income families:

- Fixed housing costs protect against inflation

- Equity building creates forced savings

- Potential for house hacking (renting rooms, ADUs, or multi-family properties)

- Downsizing in retirement can fund other goals

Education as Investment

During this period, the non-working spouse has opportunities to develop valuable skills.

- Online certifications in growing fields (digital marketing, bookkeeping, web design)

- Real estate licensing for flexible, high-earning potential

- Specialized skills that command premium rates (tax preparation, grant writing)

- Building a business slowly while family responsibilities are primary

When One-Income Living Doesn’t Work (And What to Do Instead)

Honest talk: one-income living isn’t right for every family or every season of life. Here are alternatives that provide some benefits without full transition:

Part-Time Solutions

- Job sharing: Two people split one full-time position

- Freelance or contract work: Higher hourly rates with flexible schedules

- Seasonal employment: Work intensively part of the year and focus on family the rest of the year

- Remote work: Eliminate commuting costs and gain flexibility

Creative Dual-Income Arrangements

- Opposite schedules: One works days, one works evenings to minimize childcare

- School-year only employment: Teacher, school staff, or seasonal businesses

- Home-based businesses: Both spouses work from home with complementary schedules

Your One-Income Action Plan: First Steps to Take Today

Ready to explore whether one-income living could work for your family? Here’s your immediate action plan:

This Week:

- Use our 30 Minute One-Income Decision

- Calculate your true second-income value (subtract all work-related expenses)

- List your current monthly essential expenses

- Research health insurance options if the departing spouse currently provides coverage

- Start tracking all family expenses to identify reduction opportunities

This Month:

- Build a $1,000 starter emergency fund if you don’t have one

- Create a practice one-income budget and try living on it for two weeks

- Research debt consolidation options if you have high-interest debt

- Start developing skills for potential income streams for the non-working spouse

Next Three Months:

- Live on one income while banking the second to build emergency fund

- Pay off credit card debt aggressively

- Test budget adjustments and lifestyle changes

- Create systems for strategic shopping and money-saving routines

The Truth About One-Income Living

Our family has navigated layoffs, career transitions, military moves, unexpected expenses, and more than two decades of one-income living. The lessons in this guide come from both research and real-life experience.

Here’s what successful one-income families want you to know: it’s not about having it all. It’s about having what matters most to your family.

Yes, you might drive older cars, vacation closer to home, and think twice about purchases that dual-income families make without hesitation.

But you may also gain more time for home-cooked meals, greater flexibility when children are sick, the ability to care for aging parents, and freedom from the constant juggle of balancing two careers and family responsibilities.

The families who thrive on one income share a common trait: they approach it strategically, not desperately. They plan thoroughly, adjust gradually, build financial buffers when possible, and stay flexible about both tactics and timelines.

Your family’s financial success isn’t measured by the number of paychecks you bring home. It’s measured by how well your money decisions align with your values, priorities, and long-term goals.

One-income living isn’t the right choice for every family or every season of life. But for many households, it can provide a path toward greater financial stability, flexibility, and intentional living.

The real question isn’t whether one-income living works for everyone. It’s whether exploring the option could help your family create the future you want, on your own terms.

Ready to take the first step toward one-income living?

Try our 30 Minute One-Income Decision Calculator and discover how you can thrive on a single paycheck. With the right planning, you can build a fulfilling and financially stable life for your family.

Here’s how the calculator helps you:

- Reduce anxiety about the transition

- Gain clarity on financial feasibility

- Identify expense areas for adjustment

- Make confident work-life balance decisions

- Create a personalized roadmap for your next chapter